For this fourth edition of ValueTeddys Snap Judgements we are taking a look at Discovery, which has been suggested to me by a twitter follower. It is also a 5% position in Michael Burry’s portfolio according to Dataroma when I’m writing this.

Discovery

Ticker: DISCA

Market Cap: 20.4 b SUSD

Revenue: 10.6 b USD

Discovery is probably most known for Discovery Channel and Animal Planet, but the more general description is something along the lines of: Discovery provides paid television, free-to-air TV, broadcast TV, content licencing, and direct to consumer subscription services. In other words, they own and create content, and they also own several large networks. I won’t go deeper into all the IP and networks they own, but I suggest you give it a quick glance in the annual report.

Heading straight into the financials, we see that revenues are split between advertising and distribution. Other revenues are relatively insignificant. For FY 2020 total revenues were roughly 10.6 b USD, of which 5.5 b came from advertising and 4.8 b came from distribution. Total revenues are down from 2019 and roughly on par with 2018. The reason seems to be that the advertising revenues bounce around a fair bit, whereas the distribution revenue is relatively flat. Total costs for 2020 were just north of 8 b, which left operational income of 2.5 b. Nothing odd sticks out regarding the costs. All the costs seem to be quite stable during 2018-2020. Interest expenses have decreased from 700 m in 2018 to 650 m in 2020, and after tax earnings land on 1.2 b. I note that net income changes a lot from year to year (600 m in 2018, 2 b in 2019).

Moving on to the balance sheet, there is 12 b of equity, and 21 b in liabilities, of which 3 b is short term. The asset side contains 2 b of cash, and another 4 b in other current assets. What I don’t like seeing here is over 20 b of goodwill and intangibles. To me this looks like a rather thin balance sheet. There is lots of debt and lots of intangible assets, which I generally dislike. The total debt is 1.75 times the equity, and close to 10 times the operational profits.

Looking at the cash flow the first thing I examine in this case is how much of the operational cash flow is used to service the debt. The total operational cash flow was 2.7 b in 2020, and the total interest expense was 648 m. As far as I can tell from this brief overview of the financial statements, it seems like Discovery is revolving a lot of its debt. This is far too brief an analysis for me to evaluate if this is, or could be, problematic. It is however the first thing I would look at if I were considering buying the stock. Stuff like maturities and contingencies is probably the first thing, in order to gauge how bad a theoretical worst case could be. I’m not saying they are in trouble right now, and as long as they can keep refinancing the short term debt it seems fine. But I want to say it again, to me this looks like a stretched balance sheet. Lots of debt, and lots of intangible assets.

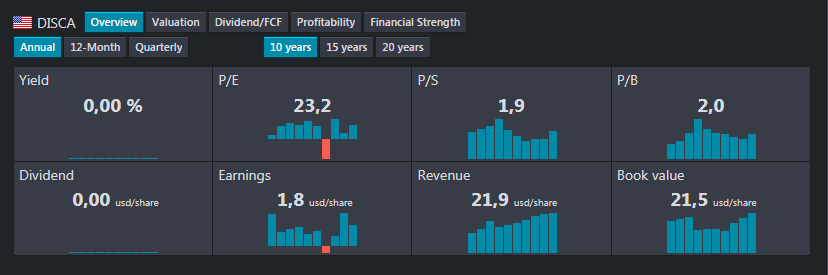

With that said, lets look at the valuation. According to Börsdata, Discovery is trading at 5x EV/EBITDA, 12x EV/Operating Cash-flow, and a P/S of 1.9. Ok so yeah, it’s looking kinda cheap. But it is actually close to its 5 year average EV/EBITDA of 4.6. Even looking back to 2011 the highest EV/EBITDA was 5.9 and lowest was 3.6. It actually traded at 4x in 2019. So it has been cheap for quite some time.

So to end this snap judgement, its not that clear cut. I don’t love the business personally, I see lots of competition to linear TV, and most of those options are better in my opinion. However, they are still earning lots of cash, and its not that expensive. They are however operating with what I deem a stretched balance sheet. Also, Dr Burry who happens to be a much smarter investor than me seems to like the stock… So do with that information what you like. I am adding Discovery to my watchlist, and I will take a harder look if they should fall to “distressed” valuation levels. I do see how many of the scenarios you can come up with seem likely. Both the doomy scenario where they simply shrink due to failure to compete with on-demand streaming services, and I see how it could be possible that they manage to keep generating cash and trade at a low multiple for some time. To summarise this case, it seems tricky, far from clear cut. Probably a good learning opportunity to try and take a good look at it, but I will put that off for now.

So that was the fourth edition of ValueTeddys Snap Judgements. I hope you liked it, and remember that none of this is financial advice and I’m not your financial adviser. If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com.