For this edition we’re taking a look at North Media, which is a case that I really like, but has a bit of troubles. However it’s a fun case to value, and somewhat decent when looking at other things. So here’s my write-up on North Media, enjoy!

Business

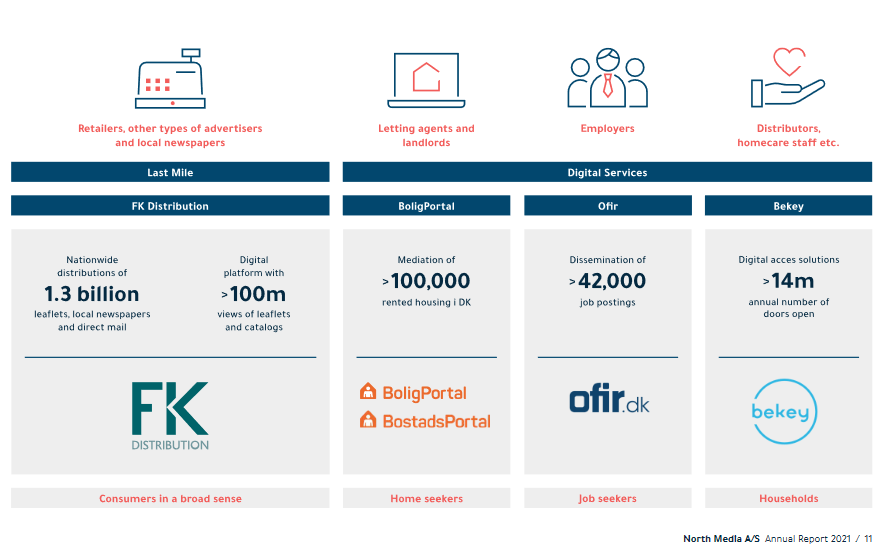

North Media can be split into two business segments, FK Distribution and Other Businesses (Digital Services). They also have a significant Stock Portfolio. I don’t see much synergies between these segments, and they are of varying quality.

FK Distribution

FK Distribution hands out advertising leaflets and local newspapers in Denmark, and they are the market leader. It also runs a digital platform called “minetillbud.dk”, and they provide logistics services. This is by far the largest part of North Media, representing about 85% of revenue and more than 90% of EBIT.

This is a quite old business, but it’s the kind that I as a value investor like. It’s better than it looks like, and if it would have been listed separately it could be traded at a very low price. I don’t think the outlook for growth here should be high, but at least it should have been done shrinking. So if it’s a melting ice cube, at least it should melt quite slowly.

Other Businesses / Digital Services

This is the segment that North Media call “Digital Services”, but that doesn’t really matter. This currently consists of three businesses: BoligPortal, which apparently is the leading home rental platform in Denmark. Ofir, which is a job postings site. and Bekey, which “delivers digital access solutions […]”.

These are all “growth initiatives”, which are good in a market that doesn’t care about profitability. I see limited benefits from these businesses being inside the North Media shell, and they would probably be worth somewhat more as standalone businesses. The most problematic business is Bekey, which has never been profitable, and in Q4 2021 caused a massive write down. The most interesting part of this bucket is BoligPortal, which is profitable and has high EBIT margins.

Stock Portfolio

Here comes the fun part, North Media has a very significant portfolio of stocks. The downside is that this portfolio has almost nothing that I would buy myself at current valuations, and I frankly value their stock picking ability very poorly. I think the S&P 500 outperforms this portfolio in the long run, especially on a risk/reward basis.

Looking at this table, we can see that as of 31.10.2022 the portfolio had taken a nice 25% haircut since year end 2021. Now you could go and adjust this for current market prices, but the truth is that I think most of these companies are quite overvalued (Or have a high risk of multiple contraction). So if I would adjust them to a multiple that I would think fair, there would be quite a discrepancy between that and the current market value.

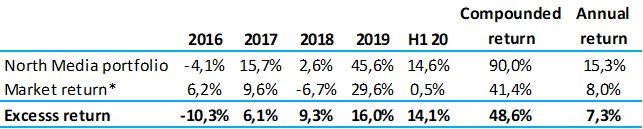

As I understand it, Mr Bunck (the founder and largest shareholder) who does the investing for North Medias portfolio. For more info on Mr Bunck, check out this text about him: http://www.northstarinvestor.com/north-media/. The text shows this picture of North Medias performance until mid 2020. and just looking at that, it seems that North Media are doing pretty well.

But looking at the portfolio it seems to me that all this out-performance is due to the insane tech bull run post the massive QE in 2020. As we saw in ‘22 a lot of this multiple expansion has been given back. Post-fact, we know that 2020 and 2021 were great years for North Medias portfolio, but ‘22 was horrible. In the Q3 2022 report, this quarterly summary is presented:

This is not adjusted for additional cash inflow into the portfolio, but I don’t think there has been much money flowing into the portfolio (nor out of it).

In short, if I got to choose between X $ in this portfolio or the same amount in the S&P 500, I would pick the latter.

Valuation

The way of valuing North Media that makes the most sense to me, is a sum-of-the-parts valuation. In all cases that are valued on a SOTP basis, a great question to ask is, why SOTP? In this case, I think it is reasonable because, the way the value would be unlocked here is by splitting out the parts. So, what are the parts worth (all figures in DKK)?

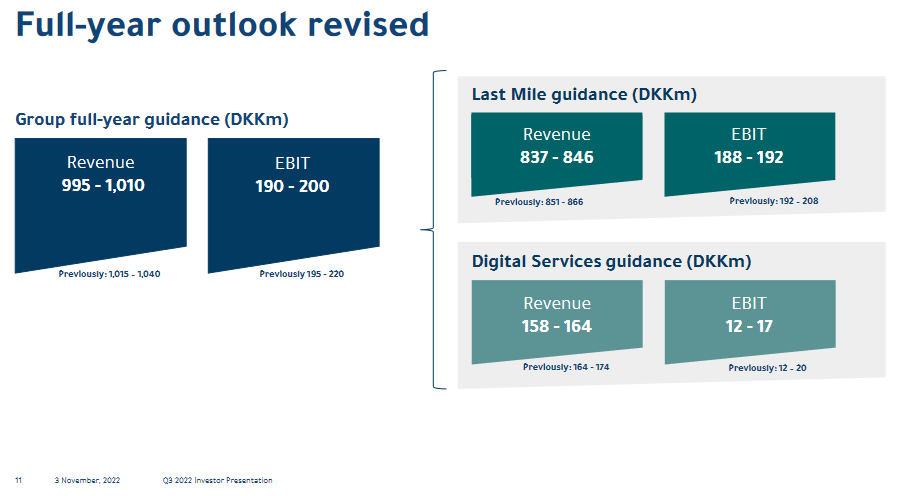

Starting with the goodies, FK Distribution. Looking at the guidance, and the fact that it’s not been growing, I think the guidance is a good EBIT level to use for valuation. Let’s call it 190m in EBIT, which I don’t think is unreasonable as an annual run rate EBIT level for FK. Given the fact that we should expect zero or slightly negative growth, lets use a small multiple. I’m going to use 6x and 8x, giving a value between 1140 m and 1520 m for FK Distribution.

The Other Businesses / Digital Services is way less important. I don’t believe them to be insanely valuable in the long run, and they take resources (time and money) from the company as a whole. Therefore I’m assigning a zero value to this part as a whole. Bekey should carry a negative value, but this is offset by BoligPortal and Ofir which at least are not burning cash. I don’t think it unreasonable to net these out against each other. If this segment only consisted of BoligPortal, the value would be above zero. Maybe something like 250-270 m (10x EBIT). If you want to be lenient you could add up to 50 m in value for the Digital Business segment as a whole.

The stock portfolio is not that valuable in the hands of North Media, as I eluded to earlier. If it were an index fund, I would use the book value, or adjust it to the current market value. But since I think this portfolio worse, it deserves a discount in my valuation. I’m using 50% discount and 25% discount, which gives us a value between 284 m and 426 m.

North Media carries about 110 m of interest bearing debt, and have about 140 m in cash, which leaves net cash of 30 m.

Combining these give us a value between 1450 m and 1976 m, or call it 1,5 b and 2 b. At 66 DKK per share, the market cap is roughly 1.3 b, which leaves a potential upside of up to 50%.

Looking at the combined picture, this should be a highly interesting situation, right? Well, yes… But there are some problems here, which leads us to the next section.

The Troubles

The first and largest problem is that I don’t think the company are allocating capital well. In fact, I think they are quite bad at capital allocation. Looking at the market cap compared to the value of the businesses (even including Bekey), it’s obvious that the company could buy back shares to create value. Looking at the stock portfolio, I think the money would be much better invested in an index, either within the company, or just paid out to shareholders (or used for buybacks). Finally, they are burning cash on Bekey which continue to lose money, and I think the outlook for Bekey is not good. The focus on new businesses and reaching for growth is ultimately not the strategy I would choose for North Media.

Just having FK Distribution and maybe BoligPortal, and then mixing dividends and buybacks for the last couple of years would have created much more value than what North Media has been doing. It should be noted that North Media has been paying dividends, and they have bought back shares, but I think this is all they should do with their free cash flow.

The second problem is that this is a controlled company. The largest shareholder (Richard Bunck) holds over 11.17 million shares, which is about 56% of the total shares. So not even with a very large wallet could you go activist on this case. This solidifies the first problem (poor capital allocation) because it makes that a permanent problem. If there were no controlling shareholder, then an activist could take a large position and begin pushing for capital allocation changes.

Wrapping it up

To wrap up things, this case is really interesting, and it should intrigue any value investor. When I first found it I made parallels to the sort of famous Buffett investment Sanborn Map, which had a large portfolio of securities as well as a good business. The differences between North Media is mainly that, when Buffett invested in Sanborn Map, the investments were carried at values that Buffett thought were significantly below fair value, and the deemed these securities to be of high quality. (See the Buffett Partnership Letters from 1960, or The Snowball). The second, and very significant, difference is that in Sanborn Map there were no large shareholders. In ‘58 Buffett put over 30% of his partnerships money into Sanborn, all of his and Susie’s money, he convinced his father to put his brokerage clients into the stock, and brokers with whom he was friendly also had clients in the stock. As I interpret the 1960 letter, Buffett held 24k shares, and together with friends etc he controlled a total of 46k shares. Buffett wanted to separate the map-business from the investments, which the board was very opposed to. Now the board and the managers together held something like less than 1k shares. The story ends well, and a plan to buy out all shareholders of Sanborn Map that wanted out. In Buffetts words: “About 72% of the Sanborn stock, involving 50% of the 1,600 stockholders, was exchanged for portfolio securities at fair value. The map business was left with over $l,25 million in government and municipal bonds as a reserve fund, and a potential corporate capital gains tax of over $1 million was eliminated.”

Unfortunately, Mr Bunck alone holds a majority of the sharers in North Media, so unless he wants out, there is no chance of going activist here. Also, since he is the one who seemingly has a hand in the existence of the stock portfolio, I see it as incredibly unlikely that it will be divested.

So, North Media can, if you squint hard enough, be seen as Sanborn Map… Except it’s worse. Sanborn had potential for control, better assets, and I think it was way cheaper.

With that said, I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser. I don’t own shares in North Media at the time, but I have owned them in the recent past and may come to do so in the future.