This post will be a quick look at Northwest Healthcare Properties, I’ll structure it like this: fist some sort of free form analysis based on the latest report Q3 2015, followed by an analysis of Earnings, Solidity and Liquidity.

Overview Northwest healthcare properties (TSE:NWH.UN) is a Canadian REIT focused on healthcare properties in Canada, Brazil, Germany Australia and New Zealand. They own a total of 123 properties, totalling 7.8 million square feet (~720000 square meters).

Northwest Healthcare properties currently pays 0.80 CAD annually, with equal monthly payments. At a price per share of 9 CAD that’s more than 9% yield. The purpose of this post is to see if that yield is safe, and if there is any kind of stability in Northwest Healthcare properties.

Looking at the Q3 2015 Report for NWH.UN they report an AFFO of 0.80 cad on an annualised basis. Because of non-recurring items the normalised AFFO is 0.84 cad. Compared to a dividend of 0.80 CAD this means they pay almost all of their normalised AFFO in dividends. Unadjusted they pay 100% of the AFFO.

They report an occupancy rate of 95.8%, this is good in my opinion. The international (non-Canadian) portfolio holds an occupancy rate of 98.1%. This combined with an weighted average lease expiry of 9.9 years means relatively safe earnings over the next 10 years. Hopefully these leases will be renewed and increasing in numbers and value.

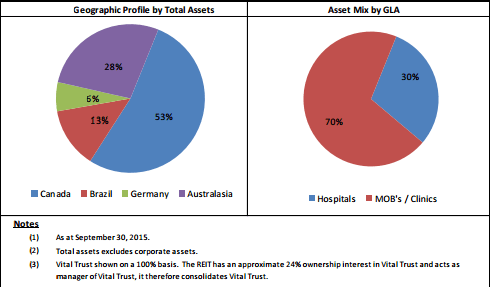

The assets are diversified as follows:

Over half of the assets are invested in Canada and 28% in Australia. The CEO utters a goal for the company to further diversify its portfolio. (“Our team looks forward to executing on this differentiated strategy as it seeks to build a leading global healthcare real estate company.” – CEO Paul Dalla Lana)

Earnings

Revenue for the nine months ending 2015 September 30 is 135 m CAD. 4 times greater than nine month ending 2014 September 30 which was 32m CAD. I take note of the big fluctuations in revenue.

Property operating costs for the nine months ended 2015 Sept 30 are 33.3 m CAD. Same period 2014 resulted in operating costs of 1.586 m CAD. Total costs are 69.4 m CAD for the same period 2015. For 2014 the total costs were 27.6 m CAD.

One reason I can see for the huge difference in revenue and costs is the merger with Northwest International Properties, NWI. This is where NWHs international portfolio comes from. The merger was completed in May 2015. (link to the press release).

FFO for Q3 2015 was 15.5 m CAD. Compared to 3.88 in Q3 2014 it a huge raise, but its also not comparable because of the merger with NWI. FFO for the nine months ended September 30 2015 landed on 26.75 m CAD.

AFFO per share after dilution for the third quarter was 0.20 CAD. for the nine months ended September 30 it was 0.61 CAD. Dividends for the same periods were 0.20 CAD and 0.69 CAD. This is a warning sign. in the third quarter they paid all of their AFFO in dividends. and for the nine months they paid more than their AFFO per share.

Solidity

The balance sheet is very much non-comparable to the balance sheet for the previous year. This is because of the merger with NorthWest International Healthcare Properties. I will do so anyway, since there might still be some information to reveal by comparing the two.

Investment properties as of September 30 2015 totals 2.5 bn CAD. per December 31 2014 investment properties totalled 524 m CAD. Quite a huge difference. 1.28 bn CAD comes from the merger with NWI according to note 8 on page 13 in the Q3 financial report. During 2015 NWH acquired all of the right and obligations of Vital Trust, and also all of NWI’s shares of NWH. These two posts make up the line Investments in Associates totalling 255.9 m CAD in Dec 31 2014.

NWH has a very small Goodwill post of 41 m CAD, this is positive since a large Goodwill post is hard to value and might indicate a larger total asset value than it actually is. I generally don’t like Goodwill. 41m compared to the property value of 2.5 bn is nothing to cause further investigation into the Goodwill post.

Liabilities as of Sept 30 2015 totals 1.75 bn CAD. As of Dec 31 2014 the total liabilities were 746 m CAD. This is also because of the merger with NWI. About 800 m CAD of debt comes from NWI.

This gives us a debt to asset ratio of 0.7 (1.75/2.5). I think this is quite high, I would like to see a debt to asset ratio closer to 0.5. However the debt is going down and the company refinanced some of the debt in the third quarter.

Annualised normalised AFFO to assets is 59.9 m / 2500 m = 0.02396, or a 2.4%. This can be seen as a return on assets, but calculated using AFFO.

NWHs Equity totals 766.77 m CAD as of Sept 30. Debt to equity is 2.28, or 228%. This means NWH has very little equity compared to the size of its total debt.

Liquidity

I calculated an annualised interest cost by taking the interest cost for the nine months ended Sept 30 2015 and adding one third of that. I ended up with 44m + 44/3 = 58.6m.

This gives us an interest coverage by annualised normalised AFFO of 59.9/58.6=1.022. Given that my calculations are correct, and that the company calculated AFFO in a reasonable manner, the interest coverage is not great.

The company has 11m in cash as of Sept 30 2015. It’s difficult to know what assets are liquid, but it seems as if they don’t have very much liquid assets. 11m in cash compared to 58 m in interest expenses is not so much.

Summary

They only offer an unaudited quarterly reports for 2015, and no annual report for 2014 yet. The report and MD&A I used were not so nice to work with. This is just some sort of gut feeling but still something I keep in mind. The website offers some investor friendliness but nothing as of multiyear overview or nice charts. I had to dig deep into the report to find the diversification of the properties.

As a financial investment NWH is risky, this is mainly because of the thin AFFO and FFO. They have a huge payout ratio of AFFO, and the AFFO barely covers their interest costs. NWH has high debt compared both to assets and to its equity.

The company is in an expansive phase, with significant acquisitions during 2015. the results of these acquisitions and the merger with NWI is crucial. They need to bump up AFFO and keep costs to a minimum.

On the bright side, the occupancy rate and the long term leases, combined with the nature of their properties, suggest steady revenue for the next 10 years.

The risks I see are in the balance sheet. The company has thin equity and not too much assets compared to its liability. Also the AFFO payout ratio is stretched, at times passing 100%.

The upside is close to 9% yield, Price to book is 1.0 (Morningstar.com at 9.13 CAD/share) expansive, not so much goodwill even though they have acquired a lot of assets during 2015.

All in all, I’m going to keep my investment in NWH.UN but I’m going to be very watchful and wait for the next quarterly report. Nortwest Healthcare Properties has potential, but also big risks.

That’s all my friends, did you like my analysis? Is there something I missed? Please tell me!

Best Regards

-Samuraimannen

Disclosure: I own shares of Northwest Healthcare Properties (TSE:NWH.UN) as I write this

Sources (PDF downloads):

Northwest Healthcare Properties website

Q3 2015 MD&A

Q3 2015 Financials (unaudited)

Morningstar