Overview

Catella is a relatively small corporate finance, real estate investment manager, and hedge/mutual fund manager focused on the Nordic market.

This is an interesting case because Catella are currently winding down some of their businesses, namely Banking (wind down to be completed in Q1-2 2021) and Catella Fondförvaltning AB (CFF). This is why Catella might be a special situation, and those can often be mispriced by the market.

Business description

Currently Catella is divided into three parts: Corporate Finance, Property Investment Management, and Funds. Catella also has a banking business which is being divested and reported separately. According to IFRS this segment is not included in group figures.

Catella are active in most of Europe, with offices also in Hong Kong and New York.

Case description

The thesis in this case is that the wind down of some of the parts in Catella can let the value in other parts of Catella be shown. With the wind down of Banking and Catella Fondförvaltning, Catella are now focusing on real estate and property management. This simplification and scaling down of business can let Catella have a better focus, which might give better future returns.

The parts in brief

Catella’s Corporate Finance department provides capital market and advisory services on property related transactions.

The Property Investment Management part focuses on property investments, offering professional investors exposure through property funds, asset management services, and through property management in the early phase of property development.

The Fund business offers actively managed funds with a focus on the Nordics, and systemic funds with a global focus. This is split into Catella Fondförvaltning (CFF) which handles the mutual funds, and Informed Portfolio Management (IPM) which deals with systematic funds.

Catella also has a banking segment that is being wound down and is being sold off since september 2018. Catella reports this segment separately according to IFRS as a disposal group held for sale.

The Parts in numbers

In the latest quarterly report, Catella reports two segments: Corporate finance, and asset management. See this formulation in the report: “Catella

has defined Corporate Finance (consisting of the Corporate Finance operating segment) and Asset Management (consisting of the combined Property Investment

Management, Equity, Hedge and Fixed Income Funds, and Banking operating segments), as the Group’s reportable segments”.

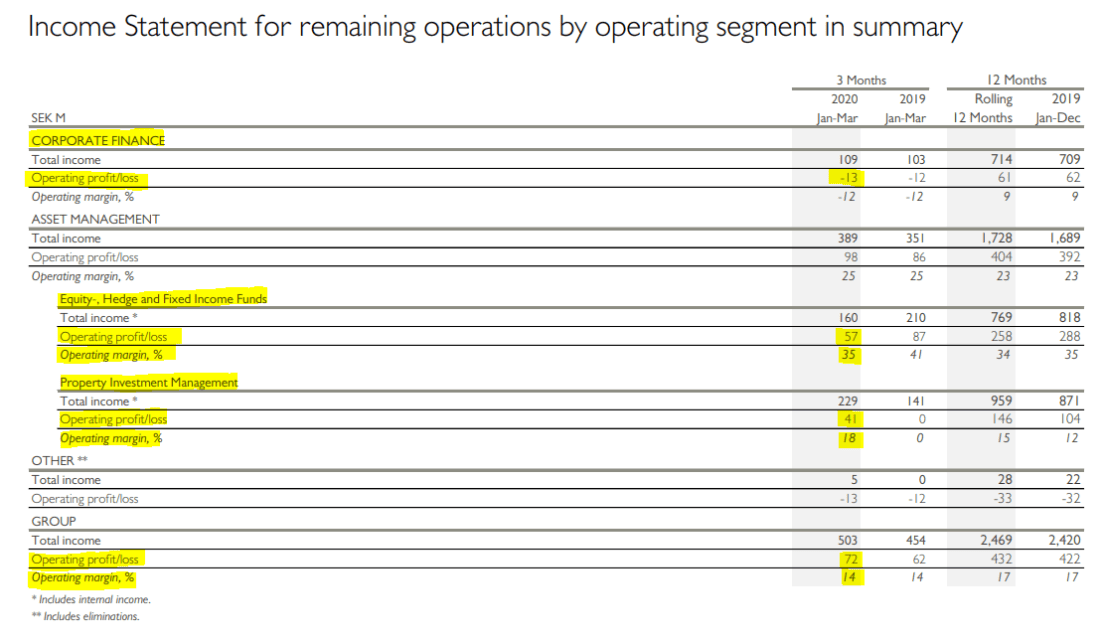

Here is a condensed income statement for the segments from the Q1 report, with some of the main points highlighted.

From this overview we see that the corporate finance carries a loss, and that the profits come from the funds and property management. Furthermore, I notice a large decline in operating profits in the fund business, that is largely compensated by an increase in the property management side.

The value of the parts

Corporate Finance

This seems like the least valuable part in Catella. It has way lower margins and several quarters with a net loss in the segment. Furthermore, CEO Knut Pedersen indicates that transaction volumes are way down in the wake of the global pandemic. Depending on how flexible Catella can be with regards to their costs in the segment, I expect the second quarter of 2020 to be very bad for Catella’s corporate finance segment. For Q2 I’m going to assume a decline in revenue in Corporate Finance of another 20%, with the same cost basis of Q1. This gives us 87 m SEK in revenues and costs of 125 m SEK, leading to an operating profit of -37.8 m SEK. Assuming some sort of return to normal for Q3 and Q4 in this segment, let’s assume 10 m in Q3 and 20 m in Q4. This lands us on an operating profit for the rest of 2020 in Corporate Finance of about -8 m SEK.

Funds

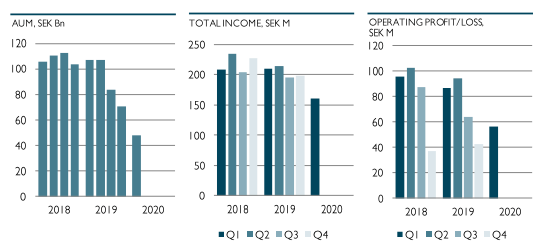

The funds also show some unfortunate signs, and in the CEOs statement Pedersen tells us that the fund segment has been seeing outflows in the first quarter. Catella had a decrease in assets under management of 23 Bn SEK in Q1, leaving them with a total AUM of 48 Bn SEK. For the fund business we are not given any guidance regarding Q2, but I am going to assume no abnormal outflows or inflows in the remaining fund business. The total income for funds totalled 57 m SEK in Q1, however the sale of CFF makes this segment really tricky.

According to the announcement related to the sale, 70% of CFF is sold for 126-154 m SEK with an option to sell the remaining 30% for 60 m SEK in January 2022. With the argument of conservatism, I’m going to assume a price that lands at 130 m and that the option is exercised. Discounting the sale price of 60 m in Jan 2022 with a 10% discount rate we get a present value of ~50 m SEK. This gives a total sale value of 180 m SEK for CFF. However the fun does not end there. Because of this transaction, a write down of 70 m SEK will be incurred in the second half of 2020. Finally, Catella expects an effect on earnings of -13 m to +15 m SEK. Again, in the name of conservatism I’m going with the lower end of this spectrum and assuming a loss of 10 m SEK. This leaves us with a one-time net effect of +100 m SEK after the sale of CFF.

Note that this sale does not include Informed Portfolio Management (IPM) which is the second fund company under the fund segment in Catella. In the Q1 report Systematic funds amounted to 100 m in revenue. applying the same operating margin for the whole segment in Q1 we should get that IPM provides 35 m SEK in operating profit. Apparently most of the decline year-over-year happened in the systematic funds, which is why I’m going to assume no growth in this segment for the remaining quarters. Note that Catella’s total ownership in IPM is 60.6%, thus the estimated operating earnings benefiting Catella are roughly 22 m per quarter for 2020.

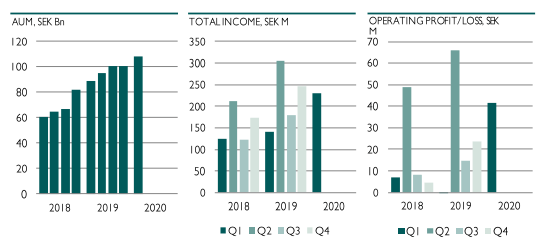

Property management

This is the only segment that shows an increase in assets under management. The AUM was 108.5 Bn SEK, an increase of 8.5 Bn since Q4 2019, and the operating profit for this segment as 41 m SEK in Q1. compare this to the same quarter last year which sported 141 m SEK in income and a big zero in operating profit. Looking at the operating profit per quarter since 2018 we can see that Q2 seems to be the significantly largest contributor to operating profit in this segment. The reasons seem to be large variable incomes from their European residential fund. I have a really hard time estimating the income for this segment, so I’m going to assume the same development for operating income as in 2019 but 20% lower in Q2 and 10% lower in Q3 and Q4. This gives us about 53 m SEK in Q2, 13.5 m SEK in Q3 and 21.5 in Q4.

One-off items are mainly the sale of CFF which is mentioned above, but also the finalisation of the wind down of the Banking segment. According to the pm that the wind-down will be completed, Catella estimated that 350 m SEK of value will benefit Catella when the process is complete, and 80 m SEK of costs will be reserved in Q2. The wind-down is estimated to be completed in the first half of 2021.

Catella also have a bunch of interesting investments on their balance sheet that should be mentioned. Consider this asset side of the balance sheet from the Q1 reports.

Some of these investments are analysed below, they are all described in Notes 3, 4, and 5 in the Q1 report.

The property developments carried on the balance sheet at a value of 428 m + 90 m SEK. There are four residential projects, three in Germany and one in Denmark, briefly summarised below:

- Name, expected transaction volume, started on, further plans/process

- Grand Central, 500 M Eur, 2015, divestment ongoing. Expected effect on Q2 earnings +155 m SEK, which i have taken into account in the estimates above.

- Seestadt MG+, 700 M Eur, 2017, producing blueprints.

- Düssel-Terrassen, 250 M Eur, 2018, producing blueprints.

- Kaktus, 130 M Eur, 2017, construction initiated, plan to finish and divest asap.

- Announced 250 m SEK investment in logistics property, estimated construction start in Sept 2020

The first thing I note is that most of these are really far out in the future. There are no time estimates, but only Grand Central seems to be under divestment currently. I am not a specialist in building, but there can probably be several years from blueprint to finished project, and in most of these projects the blueprints are not even finished.

The loan portfolio contains securitised European loans primarily exposed to housing. The portfolio is carried at a value of 123 m SEK. This loan portfolio has, as far as I can tell, not performed well at all. Out of nine loans, six have been written down to a value of zero. The remaining loans have a weighted a duration of 3.8 years. There seems to be an option for the issuer to repurchase the loans Lusitano 5 for nominal value 3.3 m EUR, which according to Catella would cause an impairment of 2 m EUR. The odds of the issuer exercising the option is estimated to increase in Q2 2021 according to Catella. I’m going to assume Catella’s assumptions are correct and that the loan portfolio is correctly valued. It should be noted that only Pastor 2 is expected to have cash flow in 2020. This stated, I assign no positive or negative value to the loan portfolio, but let it be as is. In other words, no write ups or write downs in 2020, and noting the expected 20 m SEK (2 m EUR) impairment in 2021.

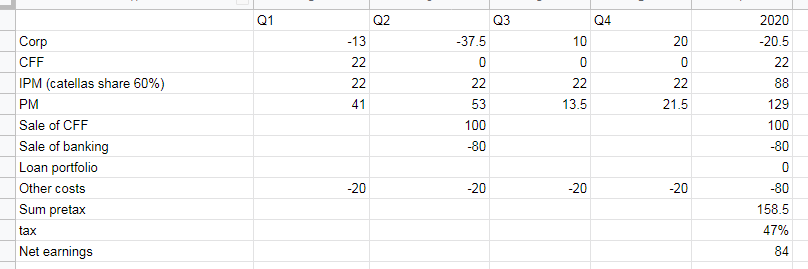

Adding it all together

Lets add everything stated above into this rough projection of operating and other profits. This gives us expected operating profits plus some one offs totalling 158.5 m SEK. Catella managed to pay an amazing 47% in taxes for 2019, and judging from the tax in the first quarter of 2020 it seems like they are still paying close to that amount. This lands us on roughly 84 m SEK of net profits for 2020. If we use a slightly lower but still high tax rate of 30% we get 111 m SEK in net profit. (Edit: The reason Catella pay such a large percentage in tax is due to gains in some countries that cant be netted against losses in other countries.)

There are way too many things that can happen before 2021, so I won’t make a prognosis that far out.

Price

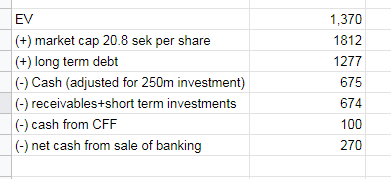

With a price per share at 21, the current market cap is 1370 m SEK, and current EV is 1120 m SEK (86.3 m shares outstanding)

EPS with 47% tax is 0.97 SEK, and with 30% tax it’s 1.28 (2020e).

This gives us P/E(2020e) 21 and EV/E(2020e) is 16 using a 47% tax rate. with 30% tax the P/E is just above 16 and the EV/E is just above 12.

Conclusion

Phew, this is a big one. First of all, some remarks: it’s messy and there are many things going on at the same time. Here is a summary list of things going on:

- Several divestments of relatively large sections of the business are ongoing.

- The property projects are really far out in the future.

- Catella are paying unnaturally high taxes.

- The Corporate finance segment is not doing that well, and should be hit very hard by Covid-19.

- The funds are seeing declining AUM.

- Lots of management changes (CEO leaves Nov 2019, CFO leaves Dec 2019, Chairman appointed CEO and a new interim CFO and a new interim chairman is appointed in March 2020. That CFO quit in June 2020.)

- Largest owner is an investment company, Claesson & Anderzén (acting CEO Johan Claesson). Other notable owners are Strawberry Capital (Petter Stordalen), and M2 Asset Management (Rutger Arnhult). Acting chairman also has stocks and bonds in Catella)

- Lots of cash and short term assets on the balance sheet (925 m cash minus 108 m pledged funds.) Also might be reduced by another 500 m due to an investment in a logistics facility announced in June. (Correction, after a short email to IR this has been clarified. Catellas part in this investment is 50%, so their investment is 250 m SEK, not 500 m SEK as I previously stated.)

The conclusion is that Catella is cheap, and that there are lots and lots of uncertainties. First the divestments have to go according to plan without incurring extra costs. Secondly, a permanent CFO and possibly a permanent CEO has to be found. Finally, the property investments have to be completed and moved to management or be sold off.

There is also the possibility that Catella can lower the very high tax-rate closer to 21,4% which is the Swedish tax rate on corporate earnings, which will have a large impact on the net earnings. Even if they reduce the effective tax rate to 30% this will have a huge effect on net earnings.

My analysis leads me to believe that there might be a turning point in the relatively near future. As more and more “non-property-related” businesses are being divested, more and more focus can be brought to refining and growing the property management business. In conclusion, Catella looks like a fairly priced bet given the current question marks, but as more and more things get figured out, the risk gets lower, and the potential upside increases. These estimates are in my view quite conservative, and with some tailwind Catella are likely to perform way better than my estimations. There are however quite some years ahead before I would label Catella a great business. If Catella manages to stabilise and build this up to start showing stable annual returns, good returns are sure to come. It’s VERY important to note that there are several stones that must fall into place before any of that can happen!

Note that my estimates and prognoses are very conservative, and a small positive deviation from my prognosis will have large effects on the bottom line. Main point is that I do not calculate the properties under development apart from the estimation made by Catella regarding Grand Central.

I think Catella is a fairly priced bet, that has large potential for future profits. However this requires good cost control and streamlining in the coming years.

I own shares of Catella, and nothing I write should be taken as financial advice, and nothing you read here should be taken as a fact. Do not make any investment decision based on what you read here, always do your own research.

Sources: Catella press releases and financial reports, Börsdata.

Some edits that have been done based on feedback:

- Catella does not own 100% of IPM, Catella owns 60.6% of IPM according to note 20 in the annual report 2019.

- I did not deduct group overhead (costs were 20 m SEK for Q1, and I’m assuming them to stay the same for the rest of 2020)

- Claesson & Anderzén is owned by the acting CEOs holding, so insider ownership is very significant.

- EV is way too high since is not adjusted for divestments

- Explanation for tax