For this weeks edition of ValueTeddys Snap Judgements we are taking a look at Plejd. A small but interesting business that has been massively popular on the Swedish part of my tweetmachine.

I want to start by recommending that you read two pieces of analysis if you find this much shorter write-up interesting.

1. @Aktiehesten (June 2020)

2. @AktieEntreprenören (April 2021)

Those two are MUCH longer and way more in-depth. They are both in Swedish so I hope Google translate can help.

Lastly before I begin, I want to remind you that the kind of write ups I do here are mainly on a “first-look” basis. They are supposed to conclude if the idea is at all worth reading up on further. It is not supposed to be as in depth as the two pieces mentioned earlier.

Plejd

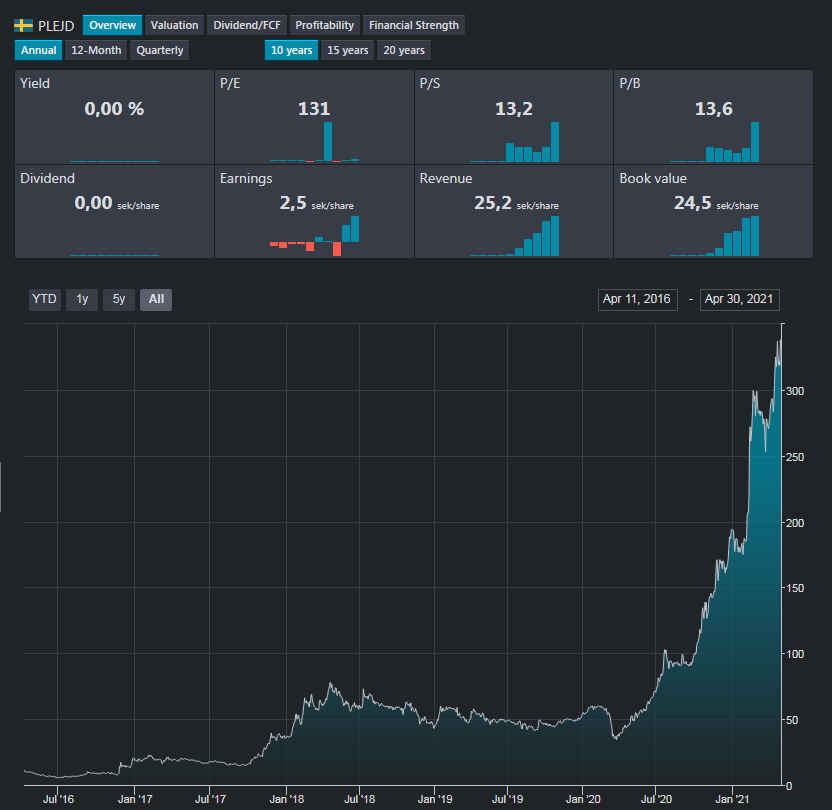

Plejd is a small swedish company, with a market cap just north of 3.5 Bn SEK, and sales of about 270 m SEK. It trades under the ticker PLEJD, on one of my least favourite stock lists Spotlight (formerly AktieTorget). As for product description, I’ll leave that to this short description on their product website: “With our comprehensive range of lighting control, we offer products for most purposes. Starting with the first product installed, you will benefit from straightforward settings and light design. As you add more Plejd products, you will experience additional advantages compared to a traditional installation. With our wireless and robust mesh technology, it’s as easy to start small and expand your system over time as it is to install a large system in your entire home or business from the start.”

Moving on to the number, I want to point out that Plejd has been a 10 bagger in just a few years. It has been almost a 10 bagger since march 2020, and it has made a massive run up since I passed on this stock after reading Aktiehestens write up in June 2020.

Looking at just the returns might be off-putting, but it seems to have been coinciding with Plejd reaching a positive net result, which is not common for growth companies in an early stage. As for financial, I’m going to look at the most recent Q1 2021 and the 2020 full year report. Figures in SEK.

It seems Plejd had a massive Q1, net revenues grew 71% from 43,5 m to 74 m with an increasing gross margin from 52% to 55% AND increasing EBIT margins from 7% to 15%. It seems easy to attribute such a massive quarter to “easy comps”, but the Q1 2020 seems to also have been a massive improvement over Q1 2019.

Looking at the income statement, Plejd does capitalise some costs, presumably development costs. This is something I generally dislike, but in this case it is not seemingly egregious, nor is it the majority of the growth. In addition to the 74 m in sales, there are 7 m of capitalised costs, and 1.7 m of other income. The reported COGS are 33 m, which leaves 41 m of gross profit. The personnel costs were 21 m and they report other external costs of about 10 m. This gives us a rough overhead of 31 m, and cash operating profit of about 10 m, or about 13% operating margins. The comparable operating profit for Q1 2020 was about 1.5 m on 43.5 m of sales. Note that this excludes capitalised costs and depreciation. Financial expenses and tax costs are low and nothing that I’d raise an eyebrow over.

This is also supported by the cash flow statement, which comes to 12.8 m in operating cf for Q1 2021 compared to 6.2 m in Q1 2020. During the quarter, 7 m was reinvested in immaterial assets, and 2 m in material assets. Another 3 m was used in paying down leasing debt. This seems reasonable, and there is nothing here that looks off.

Looking at the full year 2020, Plejd reported 209 m in sales, 93 m in cogs, ~70 m in personnel costs, and ~33 m in other overhead. In other words gross margin was 55% (116 m), and cash operating margins of about 6% (13 m). Again excluding capitalised costs and depreciation. The reported cash flow for the full year 2020 was 34 m on operations, of which 31 m was reinvested in the business (27 m in intangibles, 4 m in tangible assets). There was a capital raise of 77.7 m and about 6 m was used to pay down leasing debts.

Moving to the latest balance sheet, there is 261 m of equity and 104 m of total debt. The debt level is covered by the cash on hand of 131 m, and the company has a huge net cash position when also taking the inventory and receivables of 40 and 43 m respectively. This is a very solid balance sheet in my eyes, which is incredibly rare for such a fast growing company.

Lets get a hold of ourselves and look at the valuation. The current market cap is about 3500 m sek, and subtracting the net cash position of 112 m sek we get an EV of about 3400 m sek. This gives us the following multiples on a rolling four quarters basis: EV/S 14, EV to cash operating profit close to 160, and EV to reported cash flow from operations 88. (using the following figures rolling 4 quarters sales: 238 m, cash operating profits: 21.5 m, reported operating cash flow: 38.6 m).

On a trailing basis, this is not cheap, at all. But that does not take into account the insanely high growth rate combined with the insane feat of expanding margins, remaining cash flow positive, AND having a rock solid balance sheet with net cash. I think Plejd can keep funding their future growth without need for more external capital, and I must say that I am very impressed by their financials. I am going to exercise self restraint and not give any lofty projections based on this short analysis, but I will say that it looks like an incredibly interesting case.

This is a stock that I unfortunately have dismissed before, and thereby missing it the first time (which would have been a 10 bagger) and the second time (which would have been 6x). I won’t repeat that mistake, and I am going to read up on Plejd and it will be added to my watch list. Out of all analyses I have done in the form of these Snap Judgements, this is easily one of the most interesting cases. If you found this as interesting as I did, I must urge you to read Aktiehestens and AktieEntreprenörens write ups. And then I must strongly recommend that you do your own analysis.

That was this weeks edition of ValueTeddys Snap Judgements. I hope you liked it, and remember that none of this is financial advice and I’m not your financial adviser. If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com.