For this edition of ValueTeddys Snap Judgements we are taking a look at Kollect on Demand, a waste collection company active in the Irish and English market, listed on First North Sweden. This is a case that I have been made aware of by my favourite source of cases, Twitter, in this case @_RobinD.

Kollect on Demand

KOLL has a market cap of 140 m SEK, so this is easily what you would label as a nano cap company. Regarding what they do, this snippet is cut from the annual report 2020:

The Company services two types of customers: those who arrange to have waste collected (bins, skips and skip bags or junk removal) via the online Kollect booking engine; and those who use BIGbin smart compactor bins for waste drop-off.

The services include domestic door-to-door bin collection, commercial bin collection, skip (container) hire, skip bags and junk removal such as furniture and other large objects.

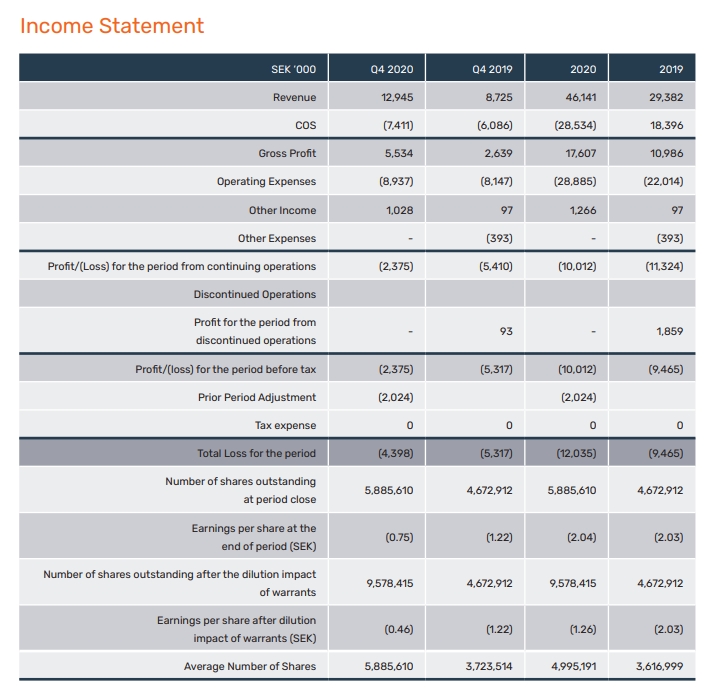

In other words, two segments; garbage collection, and larger bins for waste drop off. Something very notable is that they are founded and have the vast majority of their business in Ireland, but are listed in Sweden. Being listed in a country other than the “logical” choice is something I dislike in the absolute vast majority of cases, and this is no different. Anyway, moving to the financials. First we are taking a look at the Income statement and cash flow statement for the full year 2020 from the Q4 for 2020. Then we are looking at the Q1 for 2021. Figures in SEK.

As you can see, for 2020 KOLL had about 46 m in sales and 18 m in gross profit, up from 29 m and 11 m. The gross margins increased from less than 30% to almost 50%. The operating expenses were about 29 m, up from 22 m, leading to an operating loss.

The growth rates year on year were approximately 60% in sales and gross profits, and 30% in operating costs. Unfortunately, the number of shares outstanding after dilution doubled, leading to actual per share figures to decline. Assuming no more external equity funding needed, Kollect on Demand will be operationally profitable in three years of continued growth at this pace. I’m not so sure I believe this is the most likely scenario, but I will leave that for the concluding discussion.

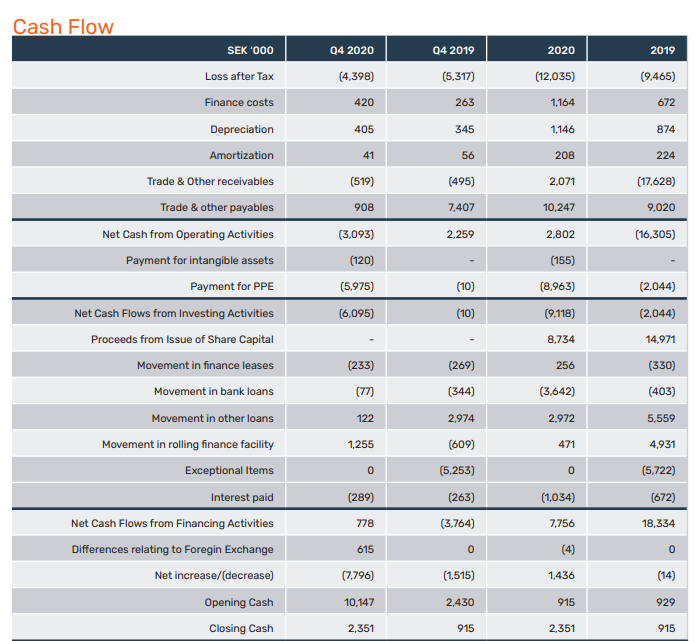

For 2020, the operating cash flow turned positive to just under 3 m, compared to a burn of 16 m in 2019. Here I note that their receivables fluctuate very significantly from 2019 to 2020, which might be something to examine further.

We see that KOLL used close to 9 m in investing in property, plant, or equipment, which was mostly funded by issuing shares. I note that significant amounts of equity capital were raised in both years. Other than that, nothing seems to be out of the ordinary regarding the financing cash flows. Moving on the the most recent quarter, Q1 2021.

For the first quarter, KOLL had 13 m in revenues, which turned into about 5 m of gross profit. Operating expenses were just above 9 m, which means an operating loss of about 4 m. Fully diluted share count was the same as in the fourth quarter. The operating cash flow was negative 3 m, no big investment was made, and bank loans increased by about 8.5 m. Sales increased about 40% and gross income about 60% y-o-y. Operating expenses increased by about 30%.

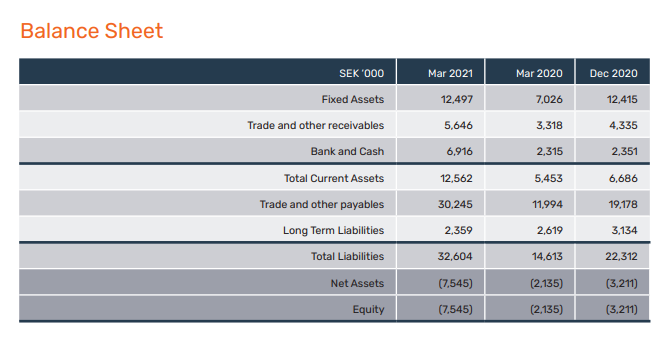

Looking at the balance sheet, there is no split of intangible assets, but the fixed assets are about 12 m, 7 m in cash and about 6 m of receivables. in total about 25 m of assets. this is funded by 30 m of short term debt and 2 m of long term debt, which leaves a negative equity position.

Summary

Okay, that was a lot of numbers, and as a summary I have to say that I don’t really see the case. The gross income has to double without operating costs increasing in order for them to make an operating profit. I think that that will require a lot of time, and because of the nature of unprofitable businesses it will require more financing. I also see a lot of debt on the balance sheet in relation to their receivables plus cash, further increasing the cause for more equity financing.

Secondly, I don’t see any kind of competitive advantage on the side of Kollect, and I don’t understand where such an advantage would come from. Without any positive cash flow, no competitive advantage, and as far as I can tell, no undervalued asset on the balance sheet, I don’t see where the upside will come from.

In defence of Kollect, they are growing at a high pace. As I touched upon earlier, continuing growth at this pace would lead to profitability in about 3 years. If we Believe this is what will happen, how many times will Kollect need to take in additional equity financing?

All this talk of further financing, leads us to the next section.

Warrants

Note that there are currently about 3.7 million warrants (TO1) outstanding, with the subscription period 9 – 20 August 2021. The warrants were issued in September 2020 and each warrant give the right to subscribe to one new share at a price settled at 70% of the volume weighted share price during July-August, but no more than 15 sek per share. This should put a roof on the price at 15 sek until the new shares are issued, and if fully subscribed should add about 55 m of equity capital.

Conclusion

Obviously, I’m not the only one to think they might need more external capital, I think Kollect also suspected it when going public and thus issued the warrants above. I think that the share price absolutely should not exceed 15 sek while the warrants are still outstanding, and the balance sheet is significantly improved given full subscription. I think the case should be re-evaluated after the summer, closer to the exercise of the warrants.

In other words, I don’t like the case currently, but I will keep an eye on it closer to the exercise of the warrants. Looking forward, even assuming full subscription of the warrants, Kollect still need to have very impressive growth numbers without operating costs skyrocketing. Can it be done? Yeah maybe, but what multiple should it be worth? Since I don’t see the competitive advantage for Kollect, I think it should not earn a high multiple if they become profitable. Lets say something like 6 times operating profit. What that might be, and WHEN and IF that will be, I’ll leave up to you.

I hope you liked this edition of ValueTeddys Snap Judgements! Remember that none of this is financial advice and I’m not your financial adviser. If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com.