For this weeks edition of ValueTeddys Snap Judgements we are taking a look at Facebook. The F in FAANMG (or whichever acronym you prefer), and the BY FAR absolute dominating player in social media, of all time. Facebook seems to be a consensus buy on FinTwit, and some really smart money managers (eg. Li Lu, Tepper, Terry Smith, Sequoia, Oakmark, Klarman, Bill Miller, and Loeb.) seem to hold the stock.

I assume Facebook needs no introduction, but here’s a line anyway. Facebook delivers social media and communications apps, such as Facebook, Instagram, Messenger, WhatsApp, and VR through Occulus. They make their revenues mainly from selling Ads.

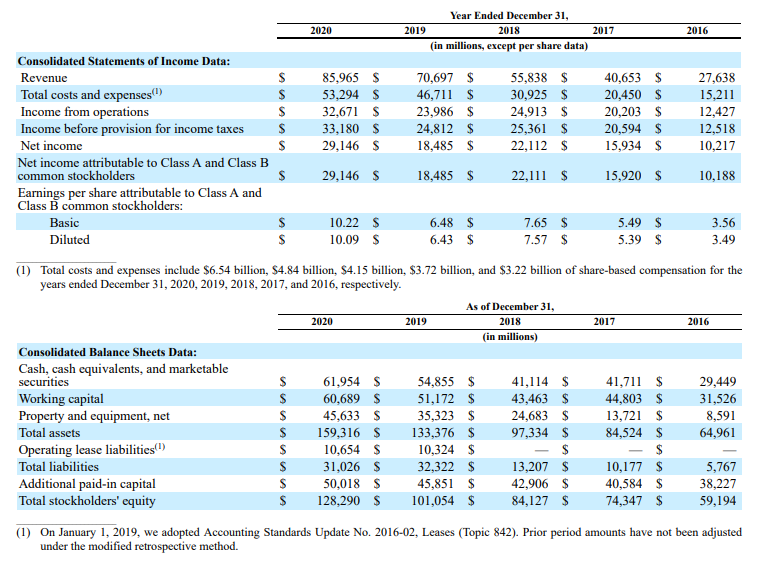

Looking at the latest 10-k (FY 2020, figures in USD), Facebook is very impressive. Total revenues were close to 86 B, and net income was 29 B. That’s a net income margins of over 33%. They also shows incredible growth each year, both in revenues and earnings. Revenue per share has grown by between 20% and 50% per year since 2012, and net earnings have grown by over 20% per year except for 2012 and 2019, which both showed negative growth in earnings per share.

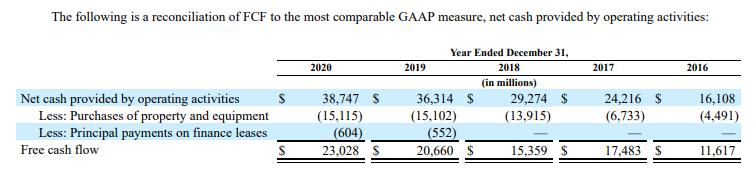

Looking further, we see amazing cash conversion, where operating cash flow and free cash flow follow the development in the income statement. For 2020, 86 B of revenue turned into 38.7 B of operating cash flow and 23 B of free cash flow. In other words, Facebook had operating cash flow margins of 45% and free cash flow margins of over 26%. Even though the margins are very high, the operating cash flow margin is lower than each of the years in the above comparison, where the operating cash flow margin was between 50% and 60%. The free cash flow margin is in line with 2019 and 2018, but was much higher in 2017 and 2016.

Now looking at 2021 Q1 figures, we see that Facebook had a massive quarter. Revenue grew about 50% and operating income and net earnings grew an impressive 90% and 80%. Interesting that sales and administrative costs both stayed about the same, only R&D increased compared to the first quarter last year. The net income margin was over 30% for the quarter, a bit higher than last year. Moving to the latest balance sheet and cash flow statement.

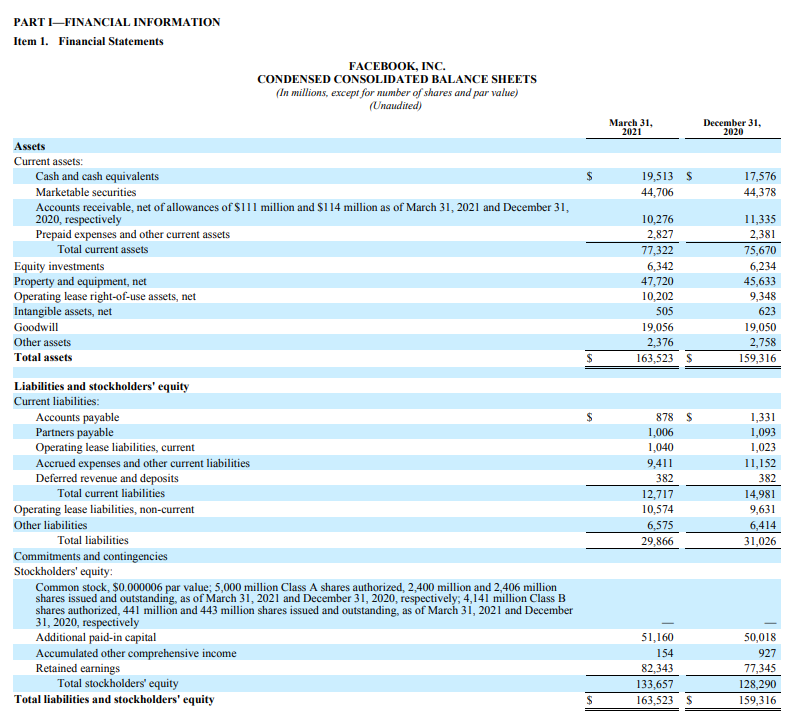

First of all, Facebook has a huge cash position at close to 20 B plus the almost 45 B in marketable securities (33 B in government securities, 11 B in corporate bonds). A surprisingly small part of the assets are made up of intangibles and goodwill, at less than 20 B, and Facebook carries almost no debt on the balance sheet, totalling less than 30 B. With over 130 B of equity, a huge cash position and very little debt, FB has an incredibly strong balance sheet.

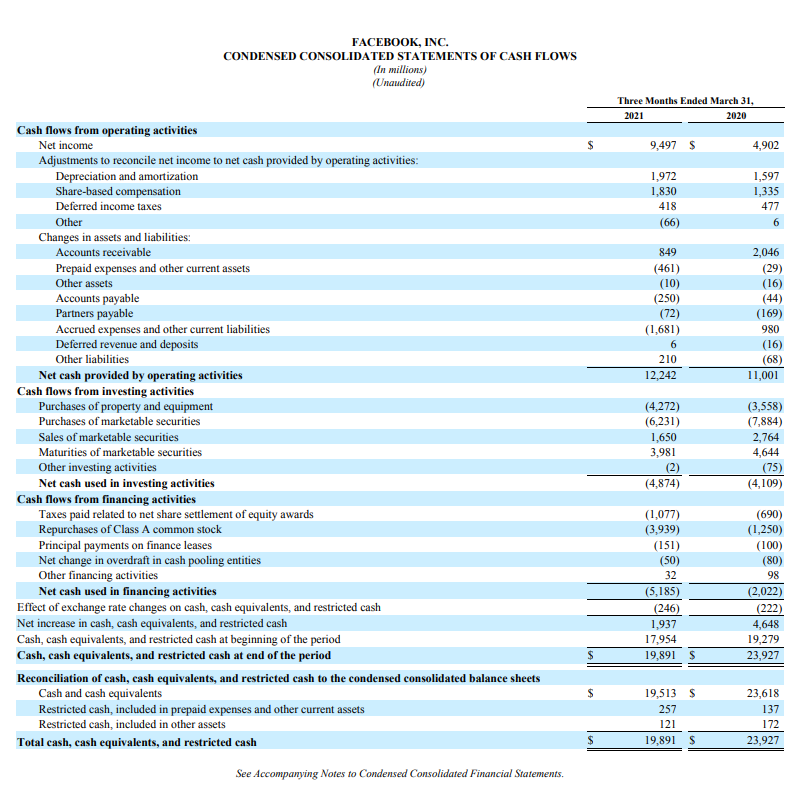

Finally, taking a look at the latest cash flow statement, we see a large portion of revenue turning into operating cash flow. 12 B of operating cash flow from 26 B of revenue gives us an operating margin of 33%, which is very high, but lower than Q1 2020 which had an impressive 64% operating margin. I also note that investment in property plant and equipment is a bit higher than last year, and that repurchases have increased significantly.

Facebook is a very interesting case, and from looking through the financials I really do see the appeal. Incredibly enough, Facebook isn’t trading at an insane valuation, at a trailing P/E of 28, EV/EBITDA 19, EV/EBIT of 23, and EV/Operating Cash-flow of 22. For the sake of brevity, I will not go in depth on all the things to consider regarding Facebook, but I will mention some things that speak against the case. In summary, these are legal risks, the fact that I dislike their products, and Mark Zuckerberg as CEO.

Now starting with the fact that most of these caveats are very personal opinions, and nothing more, here is a short discussion on the topics. First, there has been ongoing “war on big tech” from lawmakers, who have been threatening to break up the largest tech companies with claims of monopoly positions and monopolistic business practices. I don’t think there is a high chance of any of the big tech companies being split up, and therefore disregard this point entirely. Most of the FAANMG businesses are the best at what they do, and I don’t think they are negatively affecting the end customer because of their size.

Segueing from this point, I spent quite some time listening to the hearings of the CEOs of “big tech”, and Mark unfortunately strikes me as a highly unsympathetic person. I must admit, Bezos came across as quite scary, but I can’t explain it… Nadella and Cook both struck me as absolutely fantastic CEOs. I do recognise the amazing business Zuckerberg has built, but I honestly don’t think he is that good for Facebook’s image, and their reputation. I don’t know if this is at all in the cards, but I think news of Mark stepping down to chairman and letting somebody more… charismatic… take the reins as CEO. Letting someone else be the face, of Facebook, but still having the power to steer the company, would be good news. (but this is of course very loosely based on my personal thoughts, and I have no insights that are actually valuable on this point. However, I do recognise that Mr Zucc is incredibly intelligent, innovative, a visionary, and what amazingly profitable business he has built).

Now moving to the final point, I absolutely hate Facebook (now called the blue app, I think), and I also very much dislike Instagram. I only use messenger because of the insane network effects, and same with WhatsApp. Now, am I the average consumer, absolutely not. Does my opinion of the products matter, I don’t know, but I would like the case a lot more if I also liked the products. From the other side, I think it has been thoroughly proven that if you are a business and want to spend ad dollars that make you visible, you have two choices: Facebook, and Google (also Amazon, but I’m leaving that out for now). In other words, Facebook (and Google) have incredible network effects, and thus both have an incredible moat.

Buffett has an interesting quote regarding Coca-Cola, and their moat. Which goes something along the lines of “If you’d give me a billion dollars and tell me to take on Coca-Cola, I’d give you the money back and tell you it cant be done.” This is something I like to use when thinking about businesses and their moats, and in ALL of the FAANMG businesses I think you can fairly confidently say “it can’t be done”.

That went a bit on the rambling side, but I think the message is clear: Facebook seems to be an amazing business, showing incredible growth and margins with very little capital required, even tho they are so big. There are some things I’m not sure I like about the business, but I do recognise its strengths, which I think far outweigh the negatives. Disclaimer: I own Facebook in my “Cloning Portfolio”, and I am looking to add it to my main portfolio as well.

That was this weeks edition of ValueTeddys Snap Judgements. I hope you liked it, and remember that none of this is financial advice and I’m not your financial adviser. If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com.