For this edition of ValueTeddy’s Write-ups, we are taking a look at what is probably one of the more complicated business I have come across. It is SoftBank, which has become a tech giant under the visionary leadership of Masayoshi Son. SoftBank trades on the Tokyo stock exchange under ticker 9984, and there are ADRs in the US on the OTC markets under ticker SFTBY. Masa founded SoftBank in 1981, and has been its CEO ever since. Currently he is probably most famous for having a 300 year time horizon, investing very heavily in future technology such as AI, telecom, e-commerce, and semiconductors.

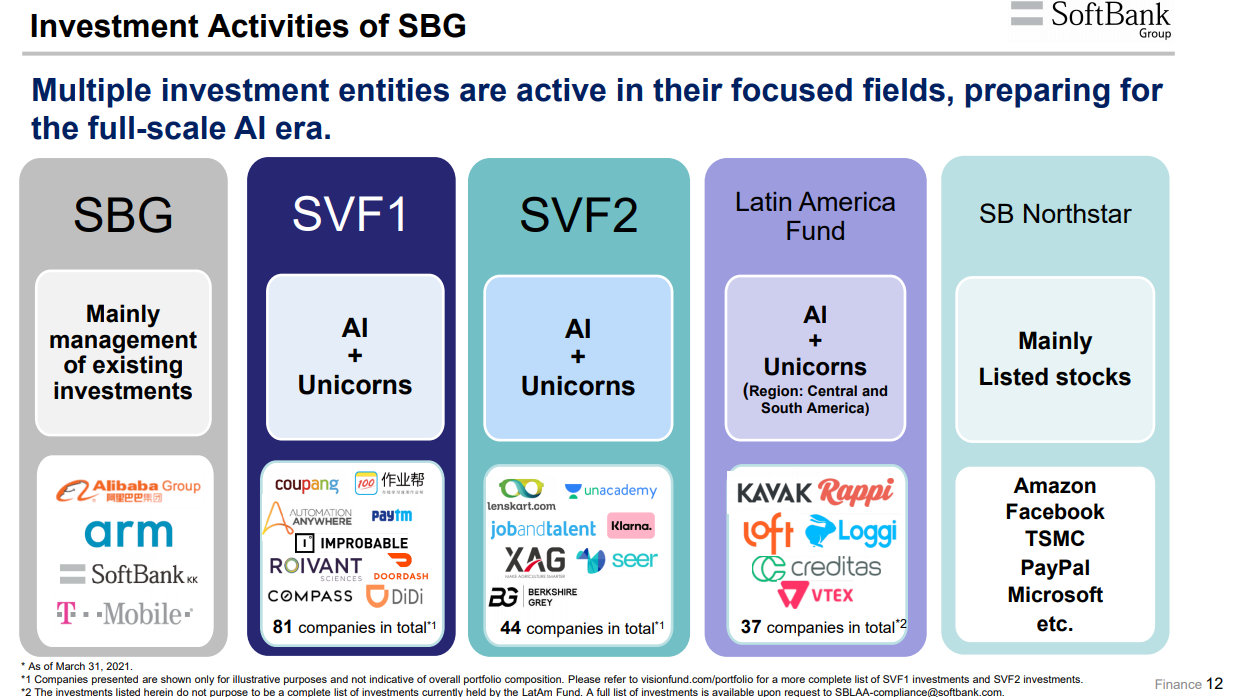

Here is an overview of the investments made by SoftBank Group, and a few examples of the assets held in each part of SoftBank.

I would describe SoftBank as a holding company or pure investment company, focusing on technology with a global scope. In their reports and on their website, SoftBank divides themselves into five parts:

- Investment Business of Holding Companies

- Vision Fund

- SoftBank

- Arm

- Other

Lets take a look at each segment.

Investment Business of Holding Companies

This segment “conducts investment activities, either directly or through subsidiaries, as a strategic investment holding company”. This segment includes holdings in approximately 110 different companies. Most notable in this segment is a huge position in Alibaba. In this segment, SoftBank also purchases derivatives, mainly call options, on listed stocks.

Vision Fund

The SoftBank Vision Fund segment might be the most well known part of SoftBank. It is made up by the two Vision Funds managed by SoftBank, and a couple of SPACs sponsored by SoftBank. According to the latest annual report SVF1 has an estimated fair value of about 120 billion USD, invested in a total of 81 companies. The SFV2 has an estimated value of 11 billion USD invested in 44 companies. SoftBank listed three SPACs, raising a total of just north of 1 billion USD. These SPACs are going to be moved away from the Vision Fund segment post merger.

SoftBank

The SoftBank segment “provides, mainly through SoftBank Corp. (ticker: 9434), mobile communications services, sale of mobile devices, fixed-line telecommunication services such as broadband services in Japan, and through Z Holdings Corporation, internet advertising and e-commerce business.” As of March 2021, one of the two “core companies” in this segment, Z Holdings, completed a merger with LINE Group. This merger was structured together with the NAVER Corporation, simplified as LINE acquiring Z Holdings, and SoftBank and NAVER each owning 50% of the new LINE Group.

Arm

“Arm’s operations primarily consist of licensing of semiconductor intellectual property (IP), including the design of energy-efficient microprocessors and associated technologies. Arm has accelerated investment in R&D by hiring more engineers. With the expansion of its engineering capability, Arm can develop new technologies that will help it maintain or increase its share of the existing markets and expand into new markets.”

In September of 2020, SoftBank proposed to sell its holding in ARM to NVIDIA in a cash and stock deal. This deal would means that SoftBank and the Vision Fund 1 will sell its entire holding of Arm to NVIDIA, more on this later.

Other

This last segment consists of three investments: SoftBank Latin America Fund, Fortress Investment Group, and PayPay Corporation.

Alternative view

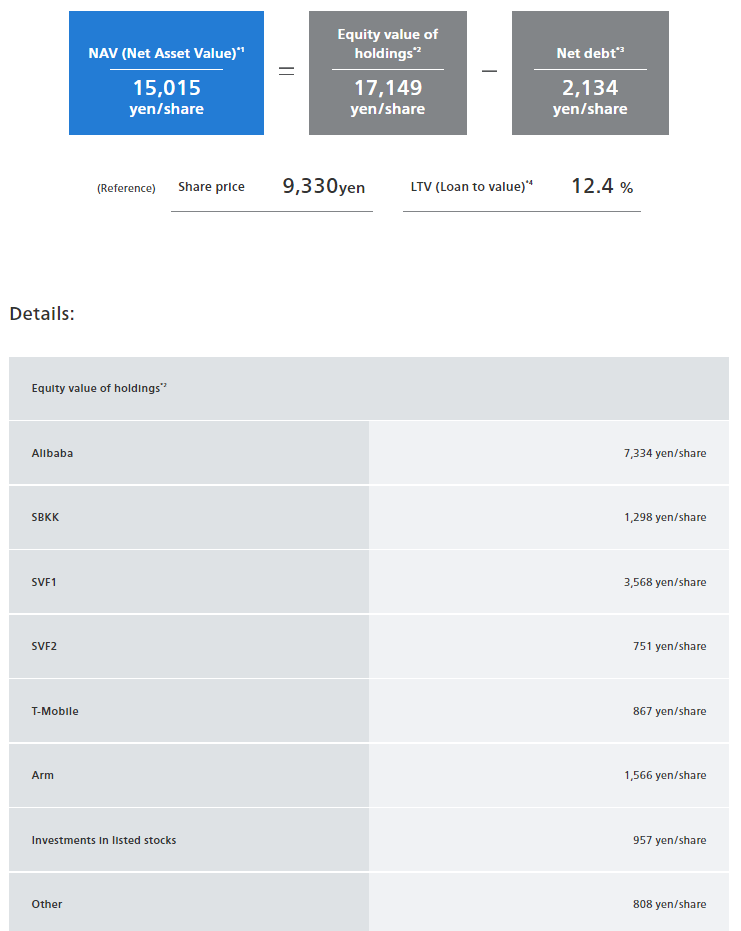

To me, this somewhat arbitrary division of segments is not the most accurate way of describing SoftBank, and I am therefore going to refer to the calculation of the net asset value published on SoftBank’s IR website as of April 1, 2021, 8:00am (JST). With this approach, we are looking at SoftBank as one single investment portfolio, with both listed and unlisted equity holdings. This is the approach that makes the most sense to me, and it lets us attempt to value the business using a net asset value approach.

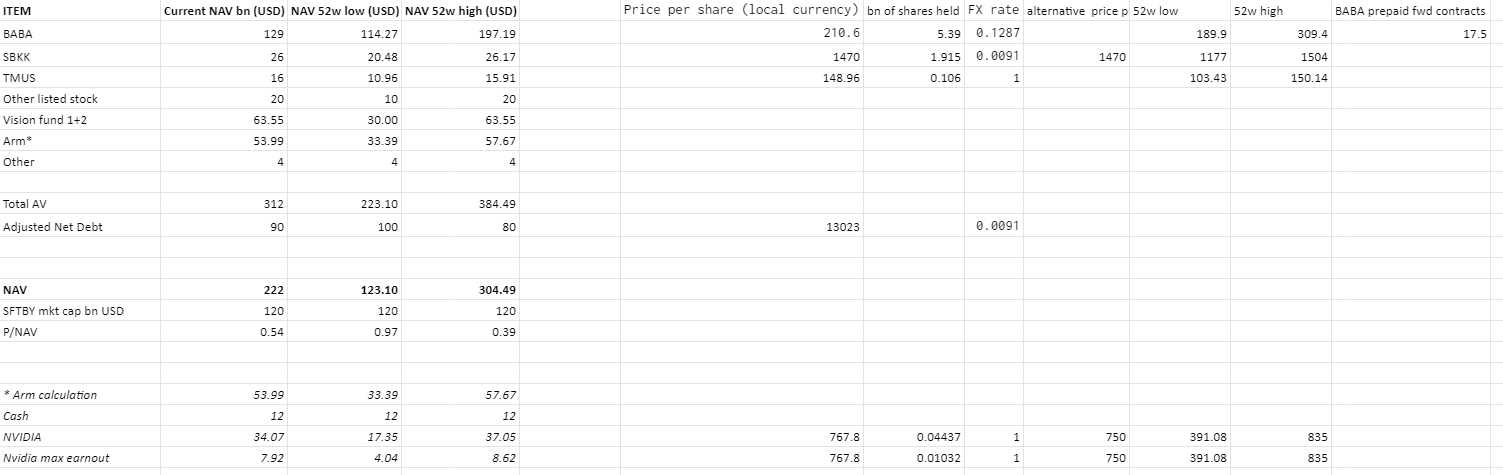

This table makes it clear that not all parts of SoftBank are equal. The holdings in Alibaba make up the majority if the NAV, and the second largest part is SFV1, followed by the holding in Arm, and SBKK (SoftBank corp). I agree with this way of valuing SoftBank, and the rest of this write-up will be my attempt to get to some sort of estimated NAV.

Alibaba

Lets start with the, by far, largest asset, a large stock holding in Alibaba. As of the latest filings, SoftBank holds about 25% of Alibaba, making them the largest owner by far. However, the calculation is made a little bit trickier because SoftBank has entered into several prepaid forward contracts using Alibaba shares.

The forward contracts are divided into two pieces, one for the fiscal year ended March 2020, and one for the fiscal year ended march 2021. The first contract will be settled in October and November 2021 and SoftBank has received 1.65 billion USD. The second contract is made up of six different contracts, each with different terms, cash amounts, and settlement dates. The contracts are roughly as follows: (in USD)

1.5 billion forward contract, settlement expected in April 2024.

1.5 billion floor contract, settlement expected in December 2023-January 2024.

8.5 billion collar contract, settlement expected in January to September 2022.

2.2 billion collar contract + call spread, settlement expected in May to June 2024.

0.9 billion and 0.8 billion collar contracts, settlement expected in July 2022 and August 2024.

In summary, SoftBank has sold a total of 17.5 billion USD worth of Alibaba shares, but the total number of shares is to be determined in the future. In order to calculate the fair value of the SoftBank holding of Alibaba shares, I think it is a fair approach to simply take the total number of Alibaba shares held and multiply by the current share price, then deduct the dollar amount prepaid on the forward contracts.

As of writing this, SoftBank holds about 5.39 billion shares of Alibaba (Hong Kong listing), multiplied by the 195 HKD closing price of Alibaba comes to about 135 billion USD using a 0.13 HKD/USD exchange rate. Deducting the prepaid forward contracts leaves us with about 117.5 billion USD of Alibaba shares.

Vision Fund 1 and Vision Fund 2

The Vision Funds (SVF1 and SVF2) are a bit easier to calculate regarding SoftBanks net asset value. SoftBank gains value from both funds in the same way, which is in two ways. First, SoftBank gains from being an investor in the funds, and secondly, SoftBank earns performance fees from both funds. Regarding the management and performance fee for SVF1 and SVF2, I won’t be taking these into consideration when estimating the NAV. The management fees are nonetheless 1%, but the performance fee is not clear to me. There are also some “claw-back provisions regarding the management and performance fee which are triggered under certain conditions […]”.

SVF1 and SVF2 are carried on the balance sheet at a total of 13.6 trillion yen. Deducting the third party interest in SVF1 of 6.6 trillion yen leaves us with a total of about 7.044 trillion yen. At the current exchange rate of 0.0091 JPY/USD this totals roughly 63.55 billion USD.

Investments in listed stocks, SBKK, T-Mobile

Starting with the holdings of SoftBank Corp, ticker 9434 on the Tokyo stock exchange. SoftBank (Group) holds about 40% of the shares in SoftBank Corp, or 1.915 billion shares. Multiplying this number of shares by the last closing price of 1450 JPY comes to a total holding of 2.777 trillion JPY, or 25 billion USD using the 0.0091 JPY/USD exchange rate.

As a part of the Sprint T-Mobile merger closing in April of 2020, SoftBank got a bunch of shares of T-Mobile. Most of these shares were sold in June 2020, but SoftBank still holds 106 million shares. At 145$ per share the T-Mobile Holdings totals 15.37 billion USD.

Finally, there is a portfolio of listed stocks, last valued at just shy of 20 billion USD. Some of the notable holdings are 6 billion USD in Amazon, 3 billion USD in Facebook, and about 1 billion USD in each of TSMC, Microsoft, and PayPal.

Arm

As I touched upon earlier, Arm is up for sale to NVIDIA in a cash plus stock deal. In the proposed deal, SoftBank and VisionFund 1 will sell the entire holding of Arm, in exchange for 12 billion USD in cash and 44.37 million shares of NVIDIA (about 33.25 billion USD at a price per NVIDIA share of 750 USD), and an earn-out of up to 10.32 million NVIDIA shares (about 7.75 billion USD at a price per NVIDIA share of 750 USD), and finally 1.5 billion in compensation for Arm employees. The maximum total value for SoftBank is about up to 53 billion USD at a price per NVIDIA share of 750 USD. This is of course highly dependent on the share price of NVIDIA . The earn-out is calculated based on certain financial targets for Arm during the fiscal year ending in March 2022.

This deal is not yet fully approved, but I think it is an okay stake in the ground regarding the potential value of Arm.

Other

Here, it is not entirely clear what exactly constitutes the “Other” in the above NAV calculation by SoftBank, so I am going to put the Latin America Fund, and PayPay in this segment. The Latin America Fund has a fair value of 4 billion USD according to the latest report, this is what am also going to use. I am going to value PayPay at 0, because it is so insignificantly small, in relation to all the other parts of SoftBank.

Net Debt

As of the latest report, SoftBank has 4.6 t JPY in cash, and another 2.2 t in receivables. They have 7.7 t JPY in sort term interest bearing debt, and 1.9 t in short term payables. There is also 10.7 t JPY in long term interest bearing debt, and 2 t in deferred taxes.

This gives us a total net debt of 15.5 t JPY, or about 141.05 billion USD using an exchange rate of 0.0091 JPY/USD. However, this significantly overstates the actual level of debt that should be used in the NAV calculation. Mainly because of the way SBKK is consolidated into the corporation. Since the negative impact of the debt is already taken into account in the equity, also counting the SBKK part of debt in the NAV should result in double counting.

Consider the following presentation slide regarding calculation of Net Debt

SoftBank starts with the total level of debt, then adjust for items they don’t think should be used when calculating the NAV. Here I am going to take the conservative route, and only deduct the items under “Net debt at self financing entities” from the “Consolidated net debt”. Therefore, I end up with a net debt of 9.46 t JPY, or 86.08 billion USD at the exchange rate 0.0091 JPY/USD. Just to be on the safer side, I am going to round this up to 90 billion USD.

Net Asset Value

That should be it, if we tally it up, we get a NAV of roughly 225 billion USD. However, much of this NAV is made up of highly volatile stocks, the value of the vision funds is made up of also very volatile underlying assets, and the potential value of Arm is highly contingent on the the price of NVIDIA shares. In other words, I am highly uncertain of the NAV 3 years from now, 1 year from now, and even 6 months from now.

This very rough table should illustrate this well enough. Here is the estimated current NAV, compared to using the 52 week high and low where it’s applicable, and adjusting some of the unlisted stuff down and up, for illustrative purposes. Using this rough method, the lowest NAV is about 164 billion USD, and highest about 300 billion USD. That’s roughly a 50% peak-to-trough.

Conclusions

At a current market capitalisation of about 120 billion USD, there is roughly a 45% discount to my estimated current NAV at 220 billion USD.

Bear case: As previously touched on, we could use the 52 week low, as well as add some discounts to some of the parts. If we use the 52 week low for each of the listed stocks, as well as discount the Vision Funds and other listed stocks by 50%, as well as increase the net debt to 100, the NAV lands approximately at 123 billion USD. At the current market cap of about 120 billion, this leaves close to zero discount.

Bull case: If we instead go off the 52 w high, and do not discount any of the other assets, we land at a NAV of about 304 billion USD. in other words, around a 60% discount at 120 billion USD in market cap.

Now, I absolutely don’t think the bull case should be trusted, as it is very aggressive, with all holdings at peak, at the same time. I also don’t think the bear case is all too scary. Even though it is very negative, assuming every major part trades at their low at the same time (something close to a crash scenario), I do think there is at least 200 billion of actual net asset value. This would be about a 40% discount, which I think is pretty good risk-reward.

Finally, I am positive on SoftBank, because I think Alibaba is looking pretty interesting right now. However, there are an abundance of risks in this case. SoftBank, and Masayoshi Son, really likes high growth companies. These are also very very expensive in almost all cases, meaning that if we see a broad risk-off sentiment, and wide range multiple contraction, most of SoftBanks holdings are going to suffer. But since Alibaba is not as egregiously prices as some other high-growth companies, I still think this looks like an interesting case. Furthermore, there is a risk that the VisionFund is full of garbage, or that some of the other investments are massive failures just like WeWork. This is a risk I am willing to take, given the risk-reward of a “VC-like” fund. Many of the investments are going to be duds, but the bet is that the very few winners are going to make up for all the losers, by a wide margin. Masa might have been insanely lucky when he struck an absolute massive home run with Alibaba, but I think there is a “non-zero chance” that Masa can pull off one or two good investments.

In short, SoftBank has many risks, but I believe the discount to NAV provides an adequate margin of safety. Do note that the SoftBank ADR (ticker: SFTBY) trades OTC, which means it might be tricky to purchase. Also note that the SoftBank shares listed on the Tokyo stock exchange (ticker: 9984) might be even trickier to purchase.

Now, this write up is gong to get some additional disclaiming. I do not currently own SoftBank, the SoftBank ADR, or anything tracking the price of SoftBank, but I may own SoftBank or any related instrument in the future. I may be way off regarding any of my calculations, so do not take anything I write for a fact. This is for informational purposes only, and it is in no way financial advice and I’m not your financial adviser.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com.

P.S Thanks @MasaSonCap, the number one authority on everything SoftBank. Huge thanks for answering my stupid questions, cheers!

Appendix

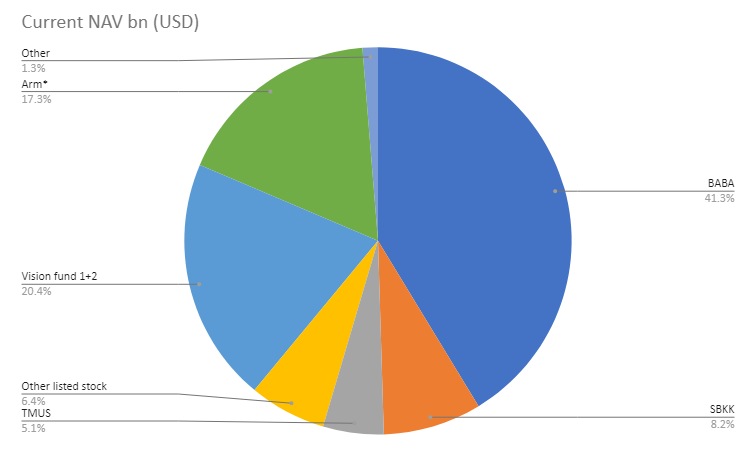

Rough graph of the asset value (ex. net debt)

Full image of my NAV calculation as of 2021-07-15

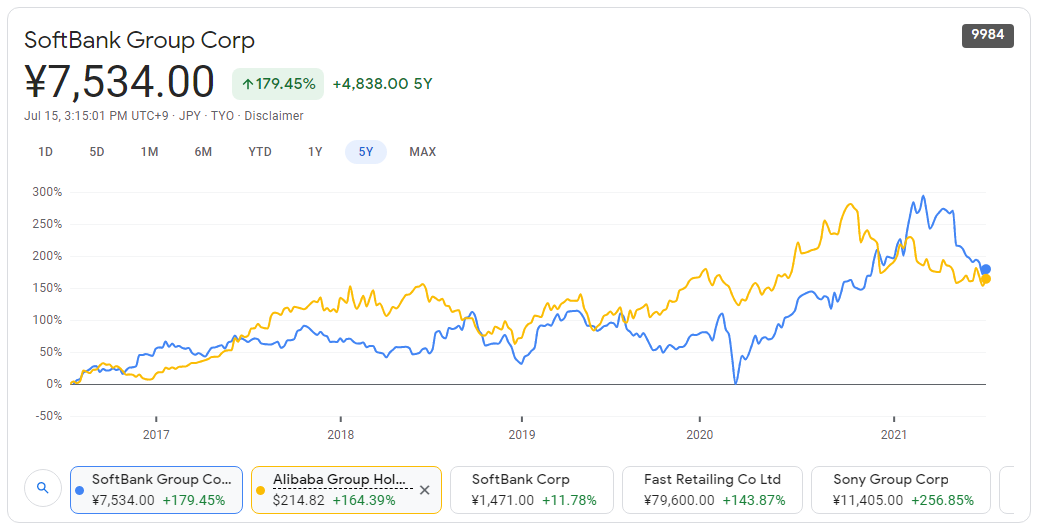

SoftBank (9984) and Alibaba (BABA) five year share price history