For this edition of ValueTeddy’s Write-ups, we are taking a look at an interesting Chinese company. First of all, I found this case purely thanks to @Olle89. Olle wrote about Sohu here in April 2021, a case I would have never came across were it not for him. I strongly suggest you read it, it’s in Swedish, but I’m sure Google Translate works reasonably well. It’s a great write-up, so I am writing this write-up purely for my own enjoyment, and to make sure I know the case to the best of my abilities.

First of all, what is Sohu? Sohu consists of three businesses, Sohu, Changyou, and Sogou. Sohu operates the following:

- Sohu Media Portal, a leading news and information provider in China, through sohu.com

- Sohu Video, an online video content service provider though the Sohu Video app, ifox, and tv.sohu.com.

- Focus, an online real estate information and services provider through focus.cn.

- Other, such as paid subscription services, broadcasting services, and sub-licensing of content.

Changyou develops and operates mobile and PC games, all with a free-to-play model with in-game purchases. The dominant game is the portfolio is TLBB, and they also own and operate the website 17173.com, which is a game related forum. Changyou was merged into the Sohu company structure in April 2020.

Finally, Sogou operate a search engine, and the Sogou Input Method, which is the largest Chinese language input software. Sogou is traded under the ticker SOGO, more on this later.

So lets look at some numbers (figures in USD).

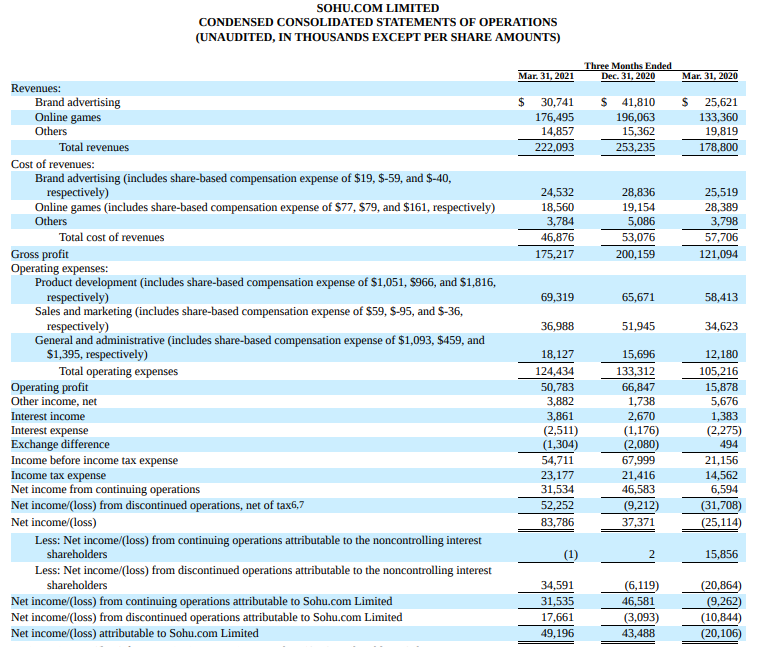

The Q1-2021 revenues was as follows: 30 m from ads, 176 m from games, and 15 m categorised as other revenue. The cost of revenues were 24.5 m for ad revenue, 18.5 m for the games revenues, and 4 m for other revenues. This gives us the following gross profits for the first quarter: 5.5 m from ads, 157.5 m from games, and 11 m from other.

The total operating expenses were 124 m, divided as 69 m to product development, 37 m to sales and marketing, and 18 m in general and administrative expenses. This leaves us with about 175 m in gross profit, and about 50 m in operating profit for the first quarter. Earnings before tax were 54.7 m in the quarter, mainly due to 3.8 m in other income, 1.3 in net interest income, and 1.3 in foreign exchange loss. The tax was 23 m, leaving 31.5 m in net income.

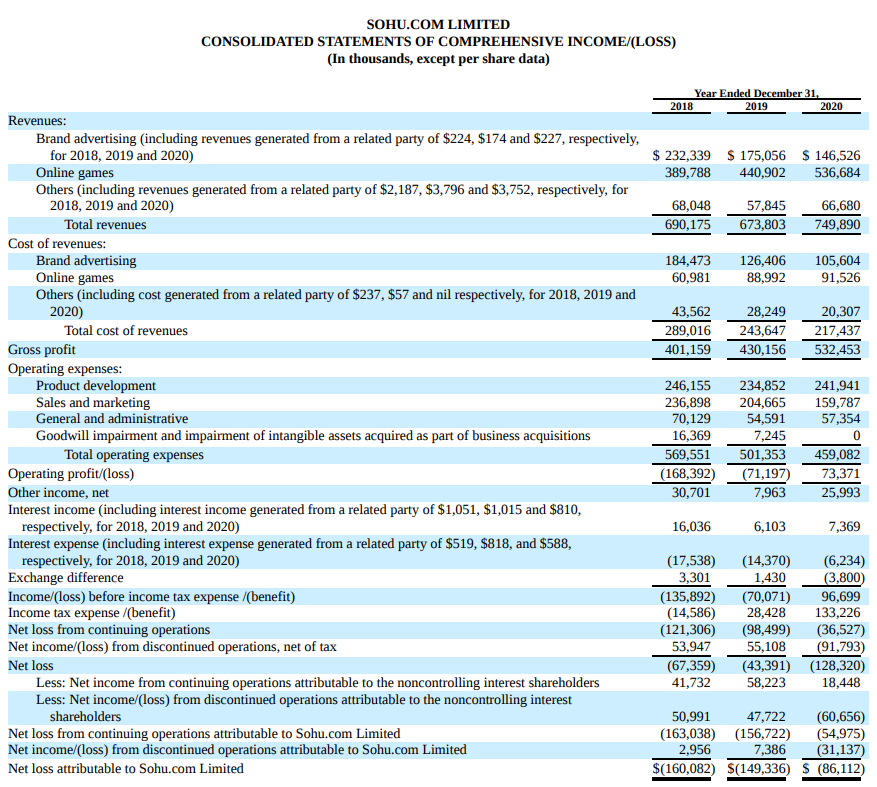

For the full year 2020, the operating income was 73 m, and income before tax was 96 m, due mainly to 25 m in other income. The tax for the full year was unusually high, at 133 m, ending the year at a net loss of 36.5 m. Compare this to the 2019 full year numbers, which shows an operating loss of 71 m, and loss before tax of 70 m. The tax expense was 28 m, bringing the net loss to about 98.5 m. The latest rolling 4 quarters amount to 107 m in operating profit and about 130 m in earnings before tax. Regarding the second quarter of 2021, Sohu is guiding for net income from continuing operations between 3 m and 13 m USD.

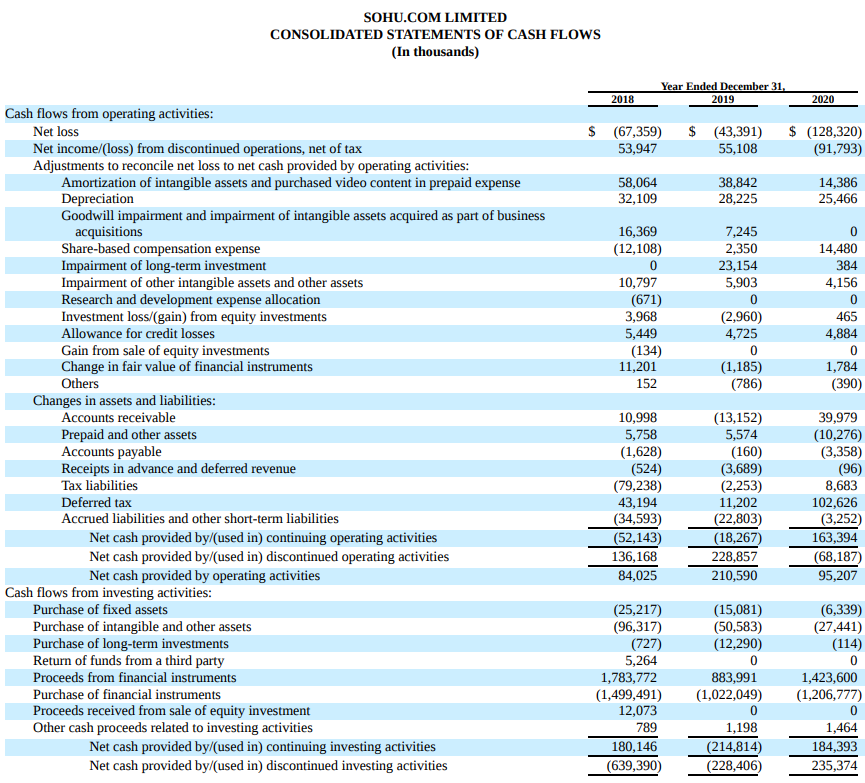

Regarding the abnormal tax expense in 2020, Sohu writes this in the annual report: “Following completion of the Changyou privatization, Changyou changed its policy for its PRC subsidiaries with respect to distribution of cash dividends. As a result, Changyou recognized an additional accrual of withholding income tax of US$88 million in the second quarter of 2020”. I don’t know how this will play out in the next quarter, nor what the exact implications are, but looking at the cash flows for the full year shows that the cash flow from continued operations were 163 m. The largest add-back was 100 m in deferred tax, which I am not sure when they will have to actually pay.

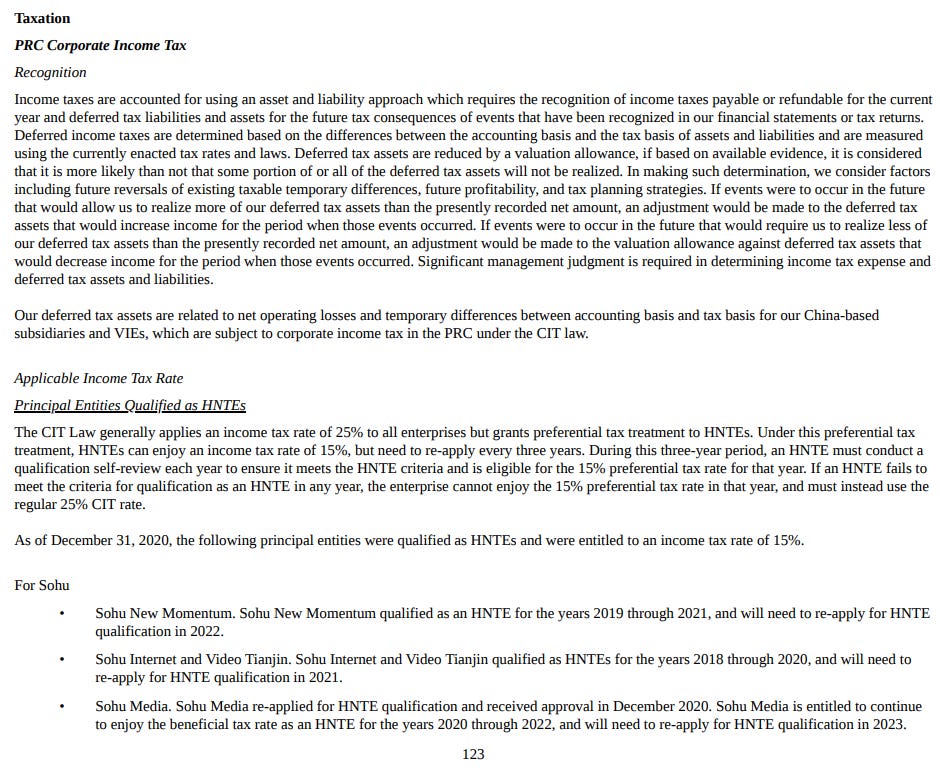

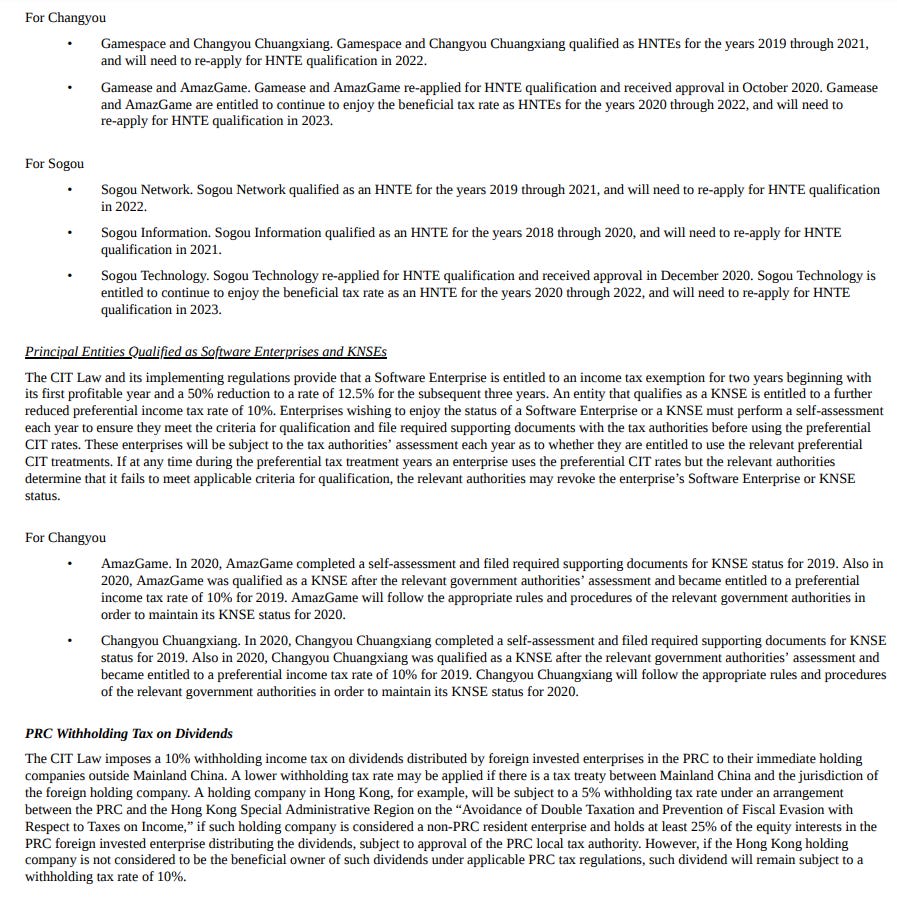

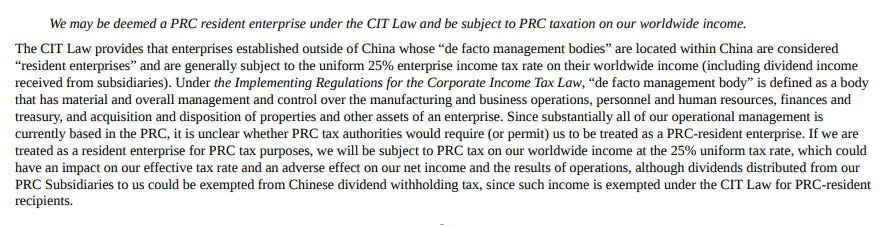

The tax situation is complicated, to say the least. This is due to them being subject to three different tax laws, US, PRC, and Cayman Islands. Furthermore, the company structure is a mix of subsidiaries and VIEs, which could potentially be problematic. I will make no attempt to pretend to understand all the tax laws Sohu has to abide to, but please see the appendix for some of the VIE- and tax related discussion in the 2020 annual report.

But, here’s the kicker to this case: these figures exclude the Sogou part of the business, since in September 2020, Sohu agreed to sell its stake in Sogou to Tencent for 9 USD per share. Since then, Sogou is reported as discontinued operations, but when this deal closes it should add 1.18 billion USD in cash to Sohu. Link to release.

Let’s take a look at the balance sheet and enterprise value.

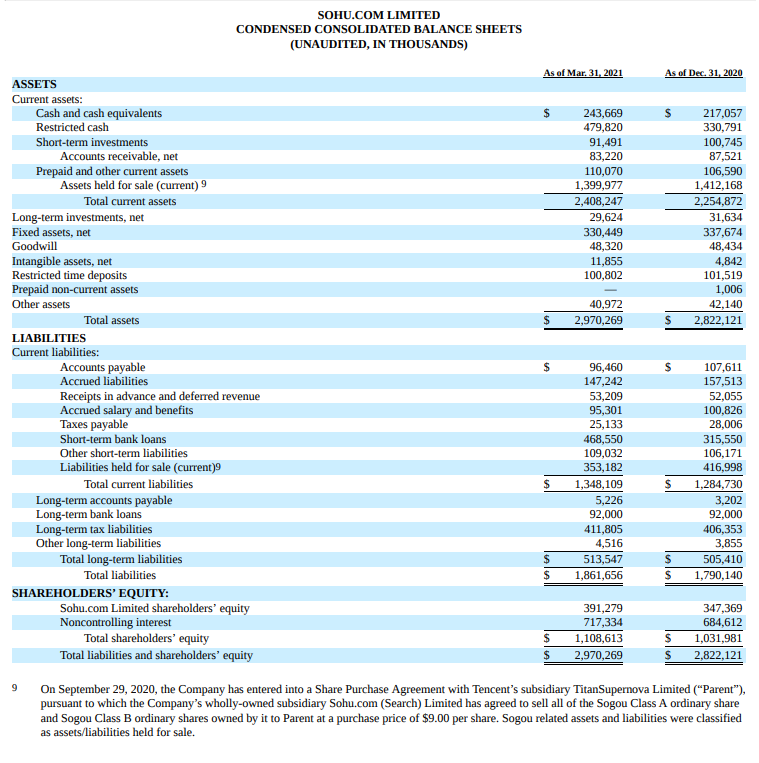

On the asset side, we’ve got 2.4 billion of current assets, and 2.97 billion of total assets. This is all financed with 1.86 billion of debt and 1.1 billion of equity. If we adjust for the assets and liabilities held for sale, and replace them with the 1.18 billion USD from Tencent, and remove goodwill and intangibles, the balance sheet becomes: 2.649 billion in assets, of which 2.188 is current assets. On the debt side we get: 1.508 billion in total debt. This gives us about 680 million of net current assets, of which 480 is held as restricted cash.

At the current market cap of about 770 m USD the enterprise value is ridiculously low, at 90 m. Even when adjusting for the restricted cash, the EV is 570 m, which is about 5x the last twelve months operating profit. Now, adjusting for this restricted cash is very conservative, as it seems they are using it coupled with the short ter bank loans. According to IR, this is in order to hold money off-shore, via depositing cash at a bank, in order to receive a loan off-shore. Thus it can be argued that if the restricted cash is adjusted out, so should the debt that it has been used as a security for. If we do that, the EV is again ridiculously low.

Conclusion

Sohu is trading close to net current assets, and its ridiculously cheap on an enterprise value basis. The business is profitable, and also growing, and they are going to have a huge cash position when the Tencent deal closes. This could be used in many different ways, for example stock buybacks, which would create huge value for the remaining shareholders at the current price. Furthermore, founder, CEO, and Chairman Dr. Charles Zhang owns about 26% of the company, so his incentives are in line with shareholders. The combination of a cheap stock, short term positive trigger as the Tencent deal closes, and founder-CEO with skin in the game leads me to think this is a great opportunity.

However, the risks are not insignificant. Mainly, the “China risk” regarding the latest crackdown on some tech companies, and further regulation regarding US listed Chinese companies. If these restrictions ramp up to the point of serious businesses being de-listed from US exchanges, or ADRs becoming worthless, then Sohu is also in trouble, along with many other serious businesses such as Tencent and Alibaba. I see this as very unlikely, but it would not be a black swan event, should it happen. All considered, I like the odds and the risk-reward.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is for informational purposes only, and it is in no way financial advice and I’m not your financial adviser. I currently hold Sohu shares, and I could add to, or sell this position at any point in time. This is absolutely not a recommendation to buy or sell anything, always do your own research.

Appendix

For a bunch of links to good references, check out Olle’s write-up.

Below are some snippets from the 2020 annual report related to taxes and the organisation structure of Sohu. It is by no means exhaustive, but the many risks are well detailed in the annual report on pages 9-65.

Taxes, pages 123-124 from the 2020 AR:

Risks related to taxation, page 31-32 from the annual report 2020:

Risks related to the offshore structure, page 28 from the annual report 2020:

On the VIE structure from pages 145-146 from the 2020 AR: