For this edition of ValueTeddy’s Write-ups, we are taking a look at the Israeli-headquartered London-listed CFD-operator Plus500. I came across this stock as I was screening for somewhat cheap stock that still show growth and profitability.

What is Plus500

Plus500 operates a platform for trading in CFDs on stocks, indices, forex, and cryptocurrencies. I think “trading” is somewhat of a euphemism in this case, and would rather call it gambling. Consider this disclaimer they are forced to have: “CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money “. So calling it trading seems unfair to trading, and gambling seems like its more appropriate.

Plus500 makes most of their money on the bid/ask spread in their products, and they are mostly active in the European market. Recently, they acquired Cunningham Commodities and Cunningham Trading Systems, effectively gaining a foothold in the US. This is a part of what they wrote in the motivations section of the acquisition announcement: “Ensure immediate access to, and the requisite licenses to operate in, the sizeable and growing US market, where the Company does not currently operate or have a presence“. Furthermore, this part of the release summarises the most important aspects of the deal pretty well: “For the year ending 31 December 2020, Cunningham generated gross revenue of approximately US$19m and profit before tax of approximately US$0.6m, with gross assets of approximately US$70m, and brings with it a scarce and valuable license to operate in the futures and options on futures market in the US”. Plus200 paid roughly 30 m USD for the entire acquisition. You can read the entire announcement here.

Financials

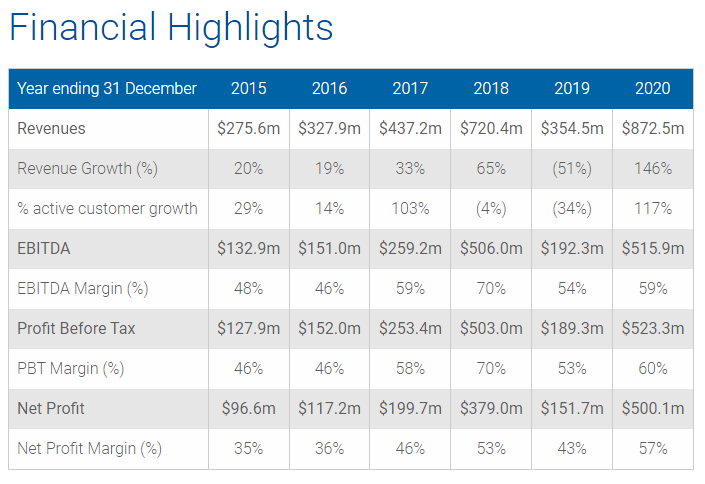

Here’s why I think this could be an interesting case: consider this financials summary from the Plus500 IR website.

We see very lumpy revenues, but the earnings margin is insanely high, through both the up- and down swings of the revenues. If that’s not enough, the free cash flow is very close to the net earnings for many of the years. In other words, there is very low capital expenditure requirements, and most of the earnings can be used either as dividends or buybacks.

In detail, the operating cash flow for 2020 was 529 m USD, and 0,3 m was used for purchase of pp&e. for 2019 these figures were 127 and 0,1. for 2018 they were 400 and 0,7, and for 2017 it was 212 m and 1m. So for the years 2020-2017, the FCF/net income was 106 %, 83.5 %, 105.5%, 55.6 %. In other words, the business is throwing off heaps and heaps of cash.

So what have they been doing with all this free cash flow? During 2020, 141 m was paid in dividends, and 89 m used in buying back shares. For 2019, the dividends were 101 m and buybacks 47 m. The 2020 buybacks were done at an average price of 12.66 GBP.

Valuation

At the current price of about 14 GBP per share, the market cap is around 1.44 B USD, and with practically no debt the balance sheet (as of 31 dec 2020), and 675 m in cash (as of the Q1 trading update), the EV is less than 1 billion USD. The total debt is 64 m, so net current assets are about 600 m, which leads us to an EV of about 840 m. Compare this to the earnings of last year, that gives us an EV/E of less than 2. If we instead compare it to the lowest earnings in the table above, the multiple is less than 9. If we use the median of the earnings in the table, the multiple is about 5.

According to the Q1 trading update, the consensus analyst estimates are about 455 m in revenues, and if I assume about 40% net margins, this gives us earnings of about 180. This in turn gives us EV/E 4.6 and P/E 8 for the full year 2021. In other words, I think the company trades very cheaply.

If we take a quick look at the listed peers IG group and CMC markets, then the P/E using the average of the last five years earnings is 7 compared to about 13 for IG and 12 for CMC. To this I should add that CMC has a similar market cap to Plus500, and IG has about the double. The EBITDA growth rate seems to be about the same for CMC and Plus500, while IG has been growing slower. But in terms of operating cash flow Plus500 by far has grown the fastest. Furthermore, the operating margin for IG is about the same as Plus500, but CMC has almost half of it in terms of percentage point margin. So at a glance, I’d say that there is no good reason as far as I can tell for Plus500 to be trading at such a high discount to these two peers.

(The image is from Borsdata.se, a service that I cannot recommend highly enough)

Closing the Price-to-Value gap

As I see it, this can be accomplished through the current 1-2 punch Plus500 is doing: buybacks and entry intro the US market. Plus500 has a stated goal to “create value for shareholders” through dividends and share buybacks. They have a history of buying back shares, the buybacks continued in the first quarter, and they have the cash to do so in size. I also think that the acquisition of Cunningham is just a first step on their attempt to take market share in the US. If they succeed, they will have gained a foothold in what’s probably one of the largest and most eager market in the world. This expansion overseas could significantly boost the growth rates, but it could also be a huge waste of money, should they fail to gain a foothold. According to the Q1 trading update, they are also focusing on increasing their product offering, to offer more than just CFDs, which could also increase growth rates.

Some of The Troubles

First, the European Securities and Markets Authority (ESMA) have been restricting CFD operators, both regarding marketing, and selling of binary options and CFDs to retail clients in the EU. This crackdown started in 2018, and in 2020 the ESMA published their final report on the matter, citing MiFID 2 and MiFIR. Before that, in 2017, BaFin restricted trading in CFDs in the German markets, and Plus500 have been fined several times in the EU. For example in a settlement with Belgian authorities in 2017, and in 2015 they had to freeze customer accounts and review their AML checks.

The AML issues in 2015 were followed by Playtech launching a bid in against the wishes of the largest shareholder Odey Asset Management. The bid was endorsed by the founders of Plus500, but the offer was in Odey’s eyes way too cheap at 4 GBP. This time Odey got their will through, and Playtech offloaded their shares a few years later, and at the current price of 14 GBP, I’d say Odey was right. However, Israeli takeover laws only require a majority vote to pass, so I do think the risk still exists that a low-ball bid could come in the future. Read more about the 2015 bid here and the capitulation by Playtech here.

Conclusion

Plus500 is looking really cheap in my opinion. Even though there are lots of risks, mostly related to regulation of CFDs, I still think the potential upside far covers the downside at this valuation.

Here’s the catch for me: most “traders”, by far, lose money “trading” CFDs, and they are often offered with very high leverage. Sure, SOME might make some money in CFDs, but the fact that CFD operators are forced to show how large percentage of their clients lose money should tell us enough. The CFD operators are encouraging people to take frequent short term bets with a lot of leverage, earning the spread on each trade. Maybe this is not as bad as gambling, but in my opinion this is much closer to gambling than investing.

That aside, if you are fine with this being basically a gambling parlour, with the front of “stock market speculation”, then I think it looks like an extreme bargain. Its wildly profitable, spews cash, and they are using it to buy back cheap shares. They also have the potential of taking market share in the US market, and they are looking to expand their products offering to more than CFDs on their platform, becoming “a global, multi-asset fintech group“. I think Plus500 could about 50% on valuation alone, and that they have good chances for continued growth with high profitability and huge free cash flows. In other words, a double whammy of multiple expansion and fundamental growth and profitability.

I have not yet decided if I want to own this kind of business in my portfolio, but I have enjoyed doing this piece of research on it. I do not own shares in any of the companies I have mentioned as I am writing this, but I might do so after this has been published.

Extra disclaimers this time: I am NOT sponsored in any way by Plus500, any CFD operator (or anyone for that matter), and I do NOT AT ALL recommend CFDs to anyone. If you want to get rich, start a monthly savings into a cheap index fund. If you want to be an investor, pick stocks, there is no need to make it more complicated than that… And for the love of god, be very very very careful with margin.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is for informational purposes only, and it is in no way financial advice and I’m not your financial adviser.

Appendix

Here are the links I used:

Acquisition announcement of Cunningham: https://otp.tools.investis.com/clients/uk/plus500/rns/regulatory-story.aspx?cid=1399&newsid=1470466

Playtech bid: https://www.valuewalk.com/2015/06/odey-blasts-playtechs-takeover-bid-for-plus500-as-opportunistic/

Playtech selling: https://www.reuters.com/article/us-playtech-plus500-sale-idUSKCN1LN0NS

ESMA CFD announcements: https://www.esma.europa.eu/search/site/cfd

Plus500 IR: https://www.plus500.com/Investors

Great writeup!

Thanks!