For this edition of ValueTeddy’s Write-ups, we are taking a look at the Norwegian holding company Wilh. Wilhelmsen Holding (WWI). The reason I came across this stock is in part due to @89Olle yet again. He told me about a very discounted value play, which is majority owned by WWI. This value play, was spun off from WWI, who still have a majority of the shares, and it might have been the stupidest reason for a spin off I have ever heard.

But first, lets take one step back, what is Wilh. Wilhelmsen Holding all about?

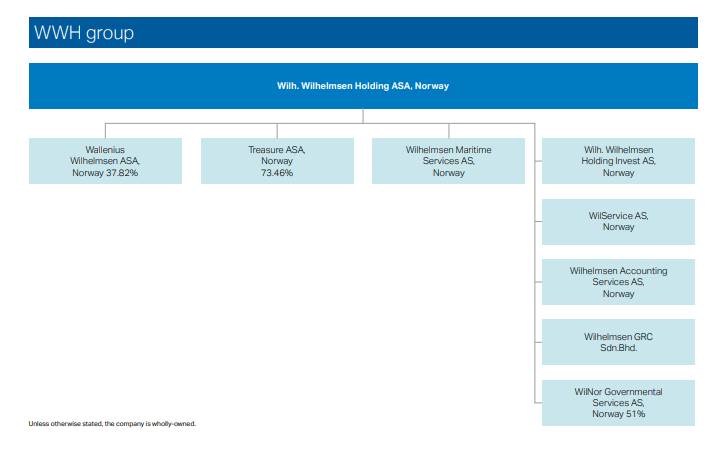

WWI is somewhat of a hodgepodge of listed and unlisted subsidiaries, but the business is divided into three parts: Maritime Services, New Energy, and Holdings and Investments. This is after quite a recent change in operating structure, and the company has undergone significant changes in the last couple of years.

Maritime Services

The Maritime Services segment contains three wholly owned subsidiaries: Wilhelmsen Ships Service, Wilhelmsen Ship Management, and Wilhelmsen Insurance Services, of which the Ships Service is by far the largest.

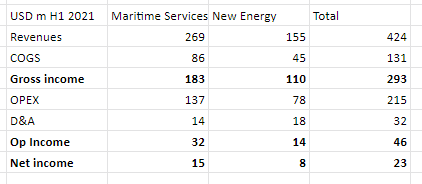

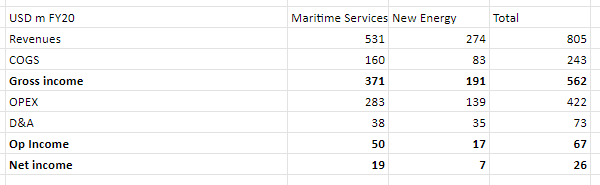

This is the largest segment with about 533 m USD in revenues and 52 m USD in operating profit for the full year 2020. These figures were 266 m USD and 28 m USD for the first half of 2021.

New Energy

The New Energy segment is divided into “NorSea Group” and “Other activities”. NorSea Group is 75% owned by WWI, and is by far the largest contributor to the segment. The Other activities part is a mess considering ownership, but here is an outline: NorSea Wind (50% owned by NorSea Group, 50% owned by Wilhelmsen Ship Management, Effectively about 87% owned by WWI), Edda Wind group (50% owned by WWI), Raa Labs AS (wholly owned), Massterly AS (50% owned), Dolittle AS (46% owned), and Other New Energy activities (whatever that means).

The New Energy segment contributed about 277 m USD in revenues, and 20 m USD in operating profit for the full year 2020. These figures were 155 m USD and 15 m USD for the first half of 2021.

Holdings and Investments

The Strategic Holdings and Investment segment includes the two listed holdings Wallenius Wilhelmsen ASA and Treasure ASA, Other Financial Investments, and Other activities.

Wallenius Wilhelmsen ASA (WAWI) is 37.8% owned by Wilh. Wilhelmsen, and is, believe it or not, a holding company in engaged in “Roll-on Roll-off shipping and vehicle logistics”. WAWI owns a large fleet of vessels in their Ocean segment, and several shipping terminals globally in the land-based segment.

Treasure ASA (TRE) is 74.8% owned by Wilh. Wilhelmsen, and has one singular purpose, holding 11% of the shares of Hyundai Glovis, listed in South Korea with ticker 086280. More on Treasure in the next section of this writeup.

Financial Investments include the groups cash and equivalents, which total about 135 m USD at the end of the first half of 2021.

Other activities is comprised of WilNor Government Services, which is owned 51% by Wilh. Wilhelmsen, and 49% by NorSea Group. and “holding company activities”. The other activities segment is very small, with and EBITDA loss of 1 m USD.

Sidebar Regarding Treasure ASA (TRE)

Before Treasure ASA was incorporated, the shares of Hyundai Glovis were held in the Wilh. Wilhelmsen holding company. However, management felt the need to “simplify the structure”, so they created Treasure, and dedicated it to hold the Hyundai Glovis position. But since WWI still owns the majority of the shares in Treasure, it is still consolidated into WWI, they still mention Hyundai Glovis in their reports, and they have not done anything material with their Treasure position. Frankly, this is one of the most confusing business decisions I have ever seen, since it further adds one layer of of complexity. In effect, Wilh. Wilhelmsen holds a listed company, Treasure, which in turn holds another listed company Hyundai Glovis. It is incredibly obvious to me that the simplest solution would be that WWI holds the shares of Hyundai Glovis. This has caused the effect that the value of the Hyundai Glovis held by Treasure, and in turn by Wilh. Wilhelmsen, are discounted by the market.

So if WWI would have held the Hyundai Glovis shares directly, as they did before creating Treasure, I would presume that the market value would be straight up added to the value of Wilh. Wilhelmsen, but instead Treasure is trading at a significant discount to the market price of Hyundai Glovis.

In short, I have absolutely no understanding of WHY Treasure exists, at all. I don’t understand if management have some ulterior motive for creating Treasure, because it does not simplify the business as far as I can tell. With that said, lets move on to the numbers.

Financials

For this writeup I am going to do a sum-of-the-parts analysis, looking at the combined value of Maritime Services, New Energy, the market value of Wallenius Wilhelmsen ASA (WAWI), plus the market value of the WWIs shares of the Hyundai Glovis shares, plus the rest of the Strategic Holdings at book value.

For the first half of 2021 the revenue, gross profit, operating profit and net income for Maritime Services and New Energy was as follows

And the full year 2020 looked like this

The current market cap for Wilh. Wilhelmsens share of Wallenius Wilhelmsen is 672 m USD at the current market cap of about 16 B NOK. (38 NOK per WAWI share)

The market cap of Hyundai Glovis at the time of writing is 6.58 T KRW. So the market value of the 11% of shares held by Treasure is 724 B KRW, or 5.56 B NOK. Since Wilh. Wilhelmsen owns 74.8% of Treasure, the market cap attributable to WWI is 457 m USD. Treasure also holds a net cash position of about 37 m USD, of which about 28 m USD would be attributable to WWI. So WWIs total net market value of Treasure could arguably be 485 m USD.

As for the balance sheet of WWI, there is about 1075 m USD of debt, of which 600 m is long term. On the asset side, excluding the book value of Treasure and Wallenius Wilhelmsen and the intangible assets, there is about 560 m USD of long term assets and 730 m of current assets. I believe these are pretty safe and defensive assumptions, leading to a large net cash position when adding in the WAWI and Treasure value.

Sidebar on the accounting, since WAWI and Treasure are both listed stocks, changes in their stock prices between the quarters will be taken as losses or gain over the income statement. Since the price of the stocks don’t always follow the value in the businesses in the short term, this causes the net earnings of Wilh. Wilhelmsen to carry less information than in other cases.

So where do we land when we put it all together?

Valuation

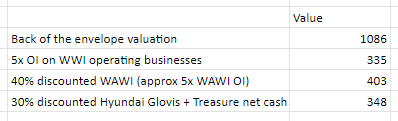

If we apply a 5x multiple on the operating income for WWIs operating businesses and on the WAWI holding, as well as a 30% discount on the Hyundai Glovis shares (WWis share of the net cash in Treasure is left un-discounted), we get a rough valuation of about 1 billion USD (9 billion NOK).

For reference, WWI and WAWI both trade at about 9x EV/OPCF on a trailing basis, and at the current share price of about 190 NOK the current market cap is about 8.8 billion NOK, or 1 b USD.

I think the first example of a 5x multiple is quite reasonable for this kind of business, because it does come with large reinvestment risks, and it is notoriously cyclical. My bet is that Wilh. Wilhelmsen is about fairly valued, but note that this valuation method ascribes zero value to everything but the WWI operations, WAWI, and Treasure/Hyundai Glovis.

More About Treasure

Let’s go back to Treasure, since I believe the whole of Wilh. Wilhelmsen to be fairly valued, but while the multiple is far lower than the market multiple there is some valuation gap somewhere. I think it lies in Treasure, and because of the structure I talked about earlier.

I am not a specialist in the Hyundai Glovis case, but when comparing the market cap of Treasure to the market value of their shares in Hyundai Glovis, there seems to be a potential for this valuation gap to close. Since valuation gaps rarely close just by themselves, there has to be something that pushes the stock price up towards the intrinsic value. In the case of Treasure, the gap has widened since its creation in 2016, but now I think that Treasure are going to actively try and close this gap through repurchases. (Note that I say “I”, but in reality this case was brought to my attention by the eminent @89Olle).

So there seems to be some uncertainties regarding Hyundai, the industrial group, and the Korean regulators want the cross holdings within the group to be resolved. Frankly, I don’t know all the details nor the implications, but as far as I understand it, Treasure has a shareholders agreement with Hyundai Glovis, so they will not just dump shares, or sell haphazardly. They are effectively partners to Hyundai, and I expect them to treat the Hyundai Glovis shares accordingly. That said, they have sold some shares, and they can sell some more while still being tax advantaged regarding dividends. Furthermore, they have a history of buying back shares, and in the most recent history these buybacks have accelerated. I believe the current discount at about 40% could be lowered to about 20%.

In my mind, it’s unlikely that Treasure sells all their shares of Hyundai Glovis and just shifts the capital over to the shareholders. Instead I think, in the long run, that Treasure will at some point invest the money into something other than Hyundai Glovis. When that is, or what that will be, is currently unknowable. However, I do like the prospects of the short term closing of the price-to-value gap in the short term, mainly spurred on by repurchases. In other words, I currently hold shares in Treasure, expecting a 20% increase in value in under 4 quarters. I think there is somewhat limited downside, unless the price of Hyundai Glovis goes down the drain. But at a trailing P/E of about 10-11 I don’t think Hyundai Glovis is grossly overvalued. Furthermore, I think it seems to be trading at a fair multiple given the steady but no-growth recent history.

Closing Remarks

I think Wilh. Wilhelmsen is an interesting case, but currently fairly priced, and I think Treasure is a fun little value play. Treasure has a meaningful gap between price and value, and it has the potential catalyst to close this gap.

I want to thank @89Olle for sharing yet another interesting case, and I want to recommend this writeup on Wilh. Wilhelmsen by the very talented Kenny of Aktiefokus. The writeup is in Swedish but I guess Google Translate would work well enough.

I hope you liked this edition of ValueTeddy’s Write-ups. If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is for informational purposes only, and it is in no way financial advice and I’m not your financial adviser. I currently don’t own shares of Wilh. Wilhelmsen (WWI), or Wallenius Wilhelmsen (WAWI), but I do own shares of Treasure (TRE).