For this edition of ValueTeddy’s Write-ups, we are taking a look at the Danish packaging company Brødrene Hartmann.

Brødrene Hartmann, headquartered in Denmark, is the world’s leading manufacturer of moulded-fibre egg packaging. They also manufacture fruit packaging, and they are also one of the world’s largest manufacturers of technology for the production of moulded-fibre packaging. In plain words, they make the cartons that hold eggs, and cartons that hold fruit. They also sell some additional services, such as branding for the egg-cartons. Finally, they also offer their production technology to other companies wanting to make packaging products. This segment is a bit counter-intuitive, to me, since it in effect turns their customers into competitors, as they offer to help them bring their packaging in-house.

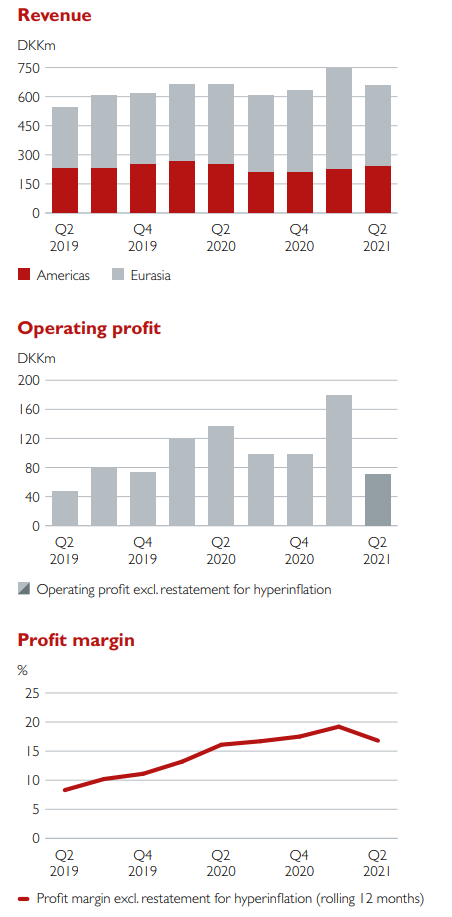

They split their geographic segments into Eurasia and Americas, where Eurasia represents about 65% of the revenues and 80% of the earnings, and this is where Hartmann are focusing most of their investments. about 400 m DKK was invested in Eurasia, compared to about 180 m invested in the Americas during the last 4 quarters.

Financials

For the full year 2020 the revenues were 2.5 billion DKK, gross profit was about 900 million, operating profit 420 m, net income 360 m, and the operating cash flow was about 450 m. For 2019 these figures were 2.36 billion in revenues, 700 m gross profit, 250 m operating profit, 215 m net income, and slightly less than 300 m in operating cash flow. In other words, 2020 was a very good year for Hartmann, due to a large increase in demand for eggs.

The latest figures as of writing are the Q2 report, which shows an increase in revenues for H1 from 1.3 billion to 1.4, but a decrease in gross profit from 485 m to 475 m. Operating income (after special items”) was unchanged at 420 m, but the net income increased from 150 m to 180 m, mainly due to significantly lower financial expenses. The operating cash flow decreased from 260 m to 225 m.

The operating cash flow margin is down to 16% from 20%, for H1 2021 compared to H12020. The gross profit margin decreased to 34% from 37%, and the net income margin is roughly unchanged at 11.5% compared to 13%.

The latest balance sheet has about 1.5 billion DKK of total debt, and the same amount in tangible long term assets. Short term assets are just shy of 1 billion , of which165 million is cash. The book value of the equity is 1.26 billion , and adjusting for non-interest bearing debt, the net non-interest bearing debt is less than 1 billion .

Overall, I think the financials of the company are pretty good. 2020 was an unusually good year, so it is not unlikely that 2021 and future years are not as good, but the operating cash flow margin is still good, and the balance sheet is solid enough.

One slight discomfort for Hartmann is the hyperinflation in Argentina, which has been a factor for their Argentinian activities since 2018. The total effect for the H1 2021 was less than 5 m DKK, but it is something to be aware of.

Other notes

Brødrene Hartmanns largest shareholder is a conglomerate called Thornico Holding A/S, who own close to 70% of the shares in Hartmann. Thornico owns several companies within food production, packaging, shipping, real estate, etc. In 2020, Hartmann agreed to deliver much of the production equipment to a new egg packaging plant in China by Thornico, and expect to receive ownership in the Chinese company. Hartmann also received an option to purchase the rest of the Chinese business two years after egg packaging production has started.

Apart from this, the nobody on the board owns a significant number shares.

Valuation

At a price per share of 400 DKK, the market cap is 2.766 billion DKK, and adding the net interest bearing debt the EV becomes about 3.5 billion DKK. This gives us an EV/OPCF of 8.5, and the P/E is about 9 using rolling 12 months OPCF. Using the full year 2019 figures, the EV/OPCF become about 12 and the P/E is roughly 16.

Compared to the 5 year operating cash flow compounded growth rate of about 10%, I think the business seems roughly fairly valued at 400 DKK per share. Given the quality of the business, and the high reliance on the egg industry, and the lack of insider shareholding, I don’t think Hartmann deserves any kind of premium valuation. Furthermore, the 2020 financials are, according to management, very positively impacted by an increased egg demand. This does not appear to be long term, so I would not be surprised to see further decline during the rest of 2021.

I bought Hartmann in late June 2020, and sold the shares in February 2021, and I could consider buying Hartmann again at a lower valuation. I currently don’t own any shares in Brødrene Hartmann.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is for informational purposes only, and it is in no way financial advice and I’m not your financial adviser.