In this edition of ValueTeddy’s writeups, we are taking a look at Havyard Group, a Norwegian marine and maritime company.

Havyard Group is a maritime company consisting of two pieces: HAV Group, and Havyard Lervik. The group has roots back to the late 30s, when the shipyard then named Løland Motorverksted was servicing and constructing vessels. In 1976 the shipyard was modernized, and in changed hands in 1979 and 1990, ending up as a part of the Kværner Group. In 2000 Havila purchased the shipyard, and founded what is currently Havyard Lervik. In 2005 a ship design company then called Leine Maritime was acquired, and turned into Havyard Design. The business grew, and in 2014 it was listed on the Oslo Stock Exchange. In 2019 the company suffered poor performance, leading to a restructuring that resolved in 2021. The restructuring resulted in the creation of a new entity, HAV Group, and a subsequent listing of its shares and a partial sale of Havyards ownership in HAV. The current structure is described briefly below.

Havyard Lervik

After the decision to discontinue the shipbuilding business the group provides repairs and rebuilds of ships through its wholly owned subsidiary Havyard Lervik. The final ship is was delivered in November 2021, and after that Havyard Lervik will only do repairs and rebuilds/modifications.

HAV Group

Havyard Group owns 66% of the shares in the public listed company HAV Group. Which in turn reports its business in four segments: HAV Design, HAV Hydrogen, Norwegian Electric Systems, and Norwegian Greentech.

This structure for HAV Group is relatively new, as it follows a restructuring described in the introduction.

HAV Design designs environmentally friendly vessels, and they claim to have a leading position in offshore wind maintenance vessels, electric ferries, and aquaculture vessels.

HAV Hydrogen is a supplier of hydrogen energy systems for vessels, both newbuilds and as retrofits.

Norwegian Electric Systems is a leading supplier of low or zero emission propulsion and control systems for vessels. They offer systems on the global market, both for newbuilds and as retrofits. For example, diesel-electric, fully electric, or hybrid propulsion systems, navigations systems, and control and monitoring systems.

Norwegian Greentech designs and implements ballast water treatment systems, which are systems designed to remove and destroy/inactive biological organisms (zooplankton, algae, bacteria) from ballast water. According to HAV, there is a large retrofit market, since regulation forces new vessels to have ballast water treatment systems, and old vessels have until 2024 to install one. Norwegian Greentech also provide solutions for land based aquaculture, such as control systems, particle filters, and UV-sterilization. Water treatment systems are an important part of land based fish farming, and HAV expects it to grow significantly.

Numbers

Here’s why this is interesting in my opinion: the market cap for Havyard Group at a price per share of 10 NOK is about 250 m NOK. The current market cap for HAV Group at a price per share of 14 NOK is just shy of 500 m NOK, which puts the value of Havyards share of HAV at about 330 m NOK.

The immediate reaction here should be to assume that HAV is grossly overvalued, but I think it might even be undervalued. Let’s look at the consolidated figures for Havyard.

Revenue for the first half of 2021 was 1.2 billion NOK, a slight decrease compared to 1.3 billion for the same period 2020. The gross profit was about 400 million NOK, an improvement compared to 360 m for the same period 2020.

Operating profit for the period was just short of 90 million, a significant increase from 54 m for H1 2020.

Net income was positively affected in H1 2021 by a one time gain on settlement of debt, and the financial expense for H1 2020 was unusually high. The unadjusted net income was 111 million NOK, compared to a net loss of close to 25 million. Adjusted for the gain on debt settlement the net income is about 64 m, and adjusted for the “other financial expense” the H1 2020 net income was about 65 million.

The reported operating cash flow was about 75 m for H1 2021, more than twice that of H1 2020 at 35 m. One weird quirk of the shipbuilding operations seems to be that they report financing related to building ships as changes in working capital, thus affecting operating cash flow (as opposed to reporting it as financial cash flow). The changes in working capital are very significant, but I suspect the figures to get smaller since the winding down of the Lervik shipbuilding operations.

A very small amount was invested in fixed assets, and about 6 m was invested in intangibles. Related to the listing of HAV Group, the company issued shares in HAV, and Havyard sold shares in HAV (resulting the the 66% ownership). The issuance of shares, and sale of shares in HAV netted Havyard Group close to 200 m, about half of which was used to pay down debt.

Restructuring 2019-2021

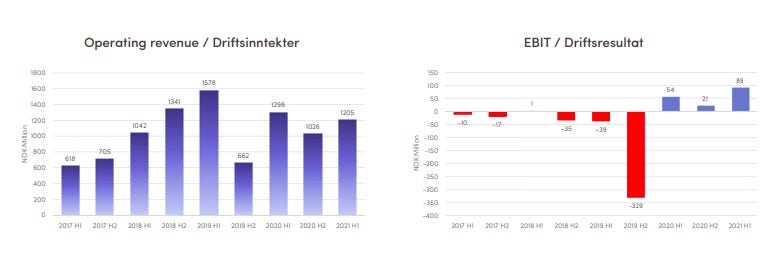

As we can see, there is nothing wrong with the latest finances, if we however take a look at the full year report for 2019, we see a huge operating loss of over 300 m NOK. See the image from the latest report.

For the full year 2019, the revenues increased, but the operating expenses increased a bit more, thus increasing the operating loss before depreciation and amortization from -90 m to -150 m. Furthermore, Havyard took a write-down of more than 150 m on non-current assets, and depreciation and amortization was more than 65 m, which is twice the depreciation of 2018. In 2018 there were no write-downs, and the depreciation and amortization was less than 30 million. Net financial expenses of about 70 m, and getting about 40 m back on taxes, moves the net loss from about -200 m to -360 m NOK.

So what caused a) the write-down of fixed assets, and b) the doubling of depreciation and amortization. And, most importantly, c) what is the risk of further restructuring and write-downs being needed in the near future?

A) The largest part of the write-down stems from the 2019 restructuring, which caused Havyard to carry out a valuation of its property, plant, and equipment. This re-evaluation of the assets led to write-downs of 122 million, with the following comment: “The impairment was driven by slower activity in the market and operational challenges at Havyard Ship Technology”. The rest of the write-down comes from Havyard writing down goodwill by about 32 million related to Norwegian Energy Systems AS.

During the restructuring, some of Havyards businesses and debt were put into Hav Group ASA, which was then listed on Merkur Market (part of Oslo Børs), allowing Havyard to sell a third of its stake, and pay down the debt on which it had breached its loan terms.

b) Looking into the depreciation and amortization we see that the depreciation on the machinery, and operating equipment are virtually unchanged between 2018 and 2019, and the a large difference stems from an increased depreciation of 30 million (compared to 8 million 2018) of Land and buildings.

Finally, c) the risk of further restructuring or write-downs… Will be dealt with under the next heading.

Risk of Further Restructuring or Write-Downs

According to the latest balance sheet (Q2), there is about 50 million in goodwill, and close to 90 million in licenses, patents, and R&D. So at worst, if the intangibles turn out to be worthless the largest write down we could see would be about 140 m (completely erasing the H1 profits, and bringing it solidly into the red). Furthermore, here is one concern, the Lervik operations used a lot of working capital. And I mean a lot. The current assets total about 1.3 billion, and the short term debt total about 1.2 billion, which is a lot compared to the 1.2 billion in revenues and operating profits of less than 100 m for H1 2021.

Looking at the segment information, we learn that about 850 m of these assets and 860 m of the debt is attributed to “Shipbuilding Technology”. I believe that the major part of this capital is due to the actual shipbuilding part of the Lervik operations. I don’t know how much of these debts and assets will be unwound as the shipbuilding business has now been would down, but I assume that more than half of the assets and debt will be unwound.

Looking at the 45 million in property, plant, and equipment, and the 34 million in right of use assets, I believe there is little chance of this being written down again, since the revaluation in 2019. However, some points that are much trickier are the hundreds of millions in receivables and customer contracts. There are currently 415 million in “other receivables” and 240 million in customer contract assets. According to a note in the 2020 annual report, “Other current receivables” contains the following line items: Prepayments suppliers, Employee-related items, Receivables VAT and government grants, Other short-term receivables. In 2020, the prepayments here were the vast majority of this balance sheet item, and I expect the same to be true for the current year.

Regarding contract assets, we have a note in the 2020 annual report for that as well: “Recognized revenue within the scope of IFRS 15 are presented as a contract asset in the balance sheet if the right to payment is conditional of future performance (usually to complete the project). If the right to payment is unconditional, the recognized amount is presented as accounts receivable. Advance payments received are presented as a reduction of the contract asset on a contract level. If advance payments received are higher than recognized revenue for a specific contract, the net is presented as a contract liability in the balance sheet. Credit loss of contract assets are similar to those for accounts receivable.” In other words, the customer contract assets are supposed to be turned into receivables, but first the company has to make some sort of performance. Contract asset liabilities are refers to payments received but not yet earned. I don’t have reason to believe that the contract assets are either overstated, nor that they will be impaired. I do however expect the size of the contract asset and liability line items to decrease in size with the winding down of Lervik.

Looking at the business, and remembering that they are fresh out of restructuring, I see the risk for large write-downs, or another restructuring to take place, as very unlikely in the coming years.

Some More Potential Troubles

Before we get to the actual valuation, I just want to note some “interesting” things that I found in the reports.

There is currently an ongoing tax case against Havyard, regarding a change of assessment regarding taxes for 2016 regarding Havyard Ship Technology AS. Havyard estimate a risk of a negative cash expense of 10 million.

More noteworthy is that there is almost a full page detailing related party transactions, something that should always be cause for detailed examination. Havyard Group is 40% owned by a group called Havila Holding AS. (Havila Holding AS has two listed subsidiaries apart from Havyard, Havila Shipping (ticker HAVI), and Havila Kystruten (ticker HKY, listed in August of 2021), and several other subsidiaries in segments such as property, media, offshore, tourism, and transport). Regarding the Q2 related party transactions, Havyard are leasing office space from Havblikk Eiendom AS. Havyard have also made sales to a company called Fjord1 ASA, totalling close to 70 million nok in Q2 2021, a figure which was more than 600 million for the full year 2020. Finally, HAV Design AS owe about 46 million to Havila Kystruten. All of these parties are owned, wholly or in part by Havila Holding AS. Related party transactions with other entities of the Havila Group are nothing new, and have been a steady occurrence in the reports since Havyard was listed.

The final point I want to bring awareness to is note 15 in the Q2 (note 26 in the annual report 2020), regarding contingencies and provisions. This also ties back to the related party Havila Kystruten, who ordered ships from a third party Spanish shipyard Hijos de J. Barreras, to which HAV Design (then Havyard Design & Solutions) had agreed to supply design and equipment. However, the relationship between Havila Kystruten and Barreras have deteriorated, and subsequently both Havyard and Kystruten sent notice of cancellation of their agreement with Barreras. Kystruten ordered the same ships but from a Turkish shipyard called Tersan Tersanecilik San. Ve Tic. A.S, and HAV Design has in 2020 entered into agreements with Tersan to sell the same designs and equipment. Related to the Barreras fallout Havyard does not expect Barreas to win any dispute case, and I presume no reservations have been made for any eventual costs related to this. I cannot seem to find the agreements under related party transactions for 2018, but they are noted in the annual report. (“[…] delivery of design and equipment to external yards that will build a total of four vessels to Havila Kystruten”). I don’t have any kind of figure regarding what potential risk here would be, but I assume (and gather from the reports) that it is not material.

Going Forward

Regarding the future income statement, in a post-shipbuilding-in-Lervik organisation, the segment information is again helpful. For H1 2021, Shipbuilding Technology provided 616 m in revenues, 21 m in operating profit. But I am going to assume that all of Shipbuilding Technology will disappear, even though the Lervik operations are wound down to only repairs and rebuilds. In relative terms, for H1, Shipbuilding Technology represents about 50% of the consolidated income, and about 20% of the operating income. Thus, the “back of the envelope restated H1 consolidated figures” are about 600 m in revenues and 70 m in operating profit. Eyeballing it, I’d say that H2 is slightly weaker than H1 (but very hard to tell in this case due to the recent restructurings), so I assume that the full year figures ex. Lervik will be something in the ballpark of 840 m in revenues and maybe 100 m in operating profit.

Price and Valuation

The most important question here is, what is it worth.

So at the current market cap of about 280 m NOK, we get an EV of about 400 m. Compare this against the trailing figures and the company looks very cheap with an EV/Operating Profit at about 3.6 (using trailing operating income of 110 m). Now incidentally, the trailing operating income is about what I expect Havyard ex. Lervik to do in operating income for 2021.

Looking at the full group consolidated (since Lervik still has been operative “as is” for the entirety of 2021), I estimate about 1.6 b in revenues and 120 m in operating income. This gives us an EV/Operating Profit about 3.33.

The final thing we could do is to note that Havyard trades at about a 23% discount to its 66% stake in HAV Group (Again using 550 as HAV market cap). On its own, HAV trades at multiples that do not look stretched at all. It has about 610 m in revenues and 56 m in operating profit for H1, and has about 40 m on net tangible assets on its balance sheet. This gives us an EV/Operating Profit of about 9 on the H1 operating profits only. (This multiple goes to 4.5 if H2 is about as good as H1)

I believe HAV can deserve a fair EV/Operating profit multiple at about 10. Now If the Havyard repair and rebuild business can remain profitable, then I don’t see why a 20%+ discount to its holding in HAV is valid. And since they are fully consolidated we don’t even have to think about discounts, but can instead think of a fair multiple on the whole business. Here I would propose that EV/Operating profit of 10 is fair, which with my previous estimates/guesses puts Havyard at 1.1 to 1.2 in EV, which means that I see pretty good upside here. Note that this multiple does not take into consideration that HAV is easily made into an ESG-case, due to their focus on sustainable solutions. I have not taken the ESG-view into consideration when determining a fair multiple for HAV or Havyard, since I personally don’t like to slap premiums onto stuff simply because it is deemed ESG, but if that is your thing then go right on ahead. (There are plenty of ESG-companies getting undefensible valuations, for example slow or no growth businesses at 20-30 times operating earnings. And if they are growing then the multiples can easily stretch beyond 50x.)

Again, this is given that none of the potential issues I raised under “going forward” and “some more troubles” does not materialize into poor operating performance.

As a final note, management does not appear in the list of largest owners, but instead Havila Holding is by far the largest owner with 40% of the shares. Furthermore, the four entities that own Havila, Emini Invest AS, HSR Invest AS, Innidimann AS and Pision AS own 5.21% each except for Pision AS which owns 1.7% of the shares. This brings the total shares under Havila/Havlia owners control to over 57%.

I currently own shares in Havyard Group.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is for informational purposes only, and it is in no way financial advice and I’m not your financial adviser.

Thank you

Hi, thank you so much for sharing the idea and your complete analysis, it really helped me to understand better the investment opportunity.

I’ve been studying the company for a while and I still have 1 concern. Everywhere I saw the estimates for 2022 for Hav Group it said it’d decrease its revenues and with it its profits from 905M of revenue in 2021 to 744M in 2022. I’ve been studying it closer and I saw that the backlog has been decreasing sharply from 2019 (the earliest year I can get the backlog data from $Hav).

In 2019 there was a backlog of 1198 (159 Internal +1039 External)

In 2020 it was 857M (99 Internal 745 External)

And at the end of Q3 of 2021, it was 638 (96 Internal+542 External)

Any idea of whether or not we should be concerned about this?

Thank you so much for your input,

Clara

Thanks for the kind words. Yes, you clearly point out the largest risk in HAV currently. If there are no new orders, I expect that they will be without anything to do sometime during the second half of 2022. For the next two reports from HAV I’m keeping a close eye on any new orders.

Thank you for your response. I will also keep a close eye on their backlog results then 😉