In this edition of ValueTeddy’s Writeups, we are taking a look at a Swedish asset management firm, and the home of “the best fund in the nordics 2020”, Namely Consensus Asset Management.

Introduction

Consensus Asset Management is a financial company based in Sweden, active in for example, wealth management, pension fund management, corporate finance, and asset management. Consensus asset management offer discretionary portfolio management to some clients, both actively managed and index-like. Their foundation management services offer full-service management of foundations, from bookkeeping, wealth management, etc. Consensus has four actively managed funds under management, they offer structured financial products, and insurance related to pensions. Finally, they partake in IPOs and M&A, and they participate as cornerstone investors and in private placements.

Consensus is very small, trades on the Spotlight market (formerly AktieTorget) in Sweden, and at a price per share of 65 sek the market cap is just shy of 500 m sek (~55 m USD), and the enterprise value is about 470 m sek.

Earnings and Cash Flow

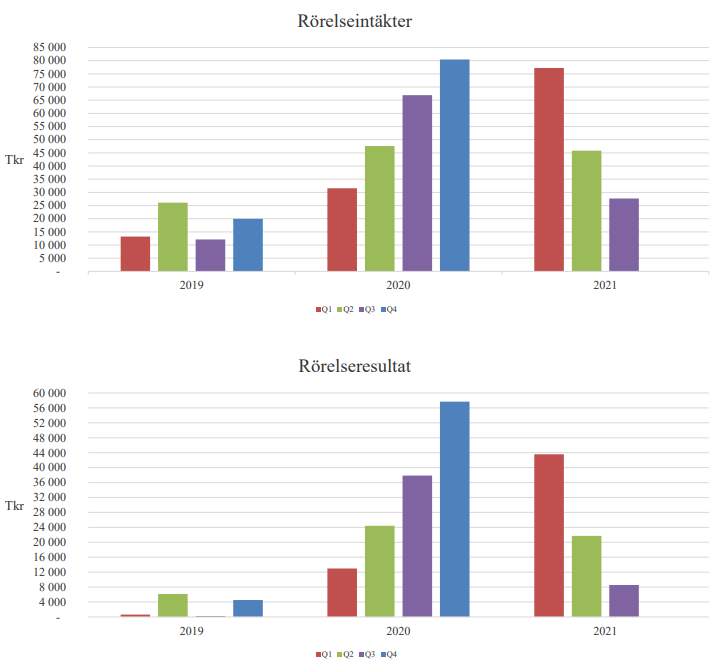

Financially, Consensus had an insanely good 2020, and the first nine months of 2021 have followed suit… mostly. The operating income (top line) each quarter in 2019 was between 10 m and 25 m sek, totalling about 70 m. In 2020 the figures for each quarter was roughly 35 m, 45 m, 65 m, and ending q1 with a staggering 80 m, making for total operating income of 225 m sek. 2021 started out strong, with about 75 m, then it promptly declined in q2, to 45 m, and then again to below 30 m, for a total of 150 m in the first nine months of 2021.

The last three years have been a rollercoaster, as is evident from the figures above, and made more clear in the below graphs of operating income and operating profit.

Looking at the last nine months, compared to the same period in 2020, the administrative expenses plus other operating costs were about 75 m, compared to about 70 m. Depreciacion was less than 1.5 m in both periods. Tax expenses was 13 m, compared to about 25 m. So operating profit for the first nine months of 2021 were about 74 m, compared to 75 m in the same period of 2020. Net income was close to 61 m, compared to close to 51 m.

Operating profit for the full year 2019 and full year 2020 were 11.5 m and 133 m sek, and the net income for 19 and 20 were 5.6 m and 78 m.

Looking at the cash flow statements, the cash flow from operations was about 28 m, compared to 32 m, again first nine months of 2021 and 2020. Consensus have no investing cash flow, and paid a dividend of almost 65 m in 2021.

Balance Sheet

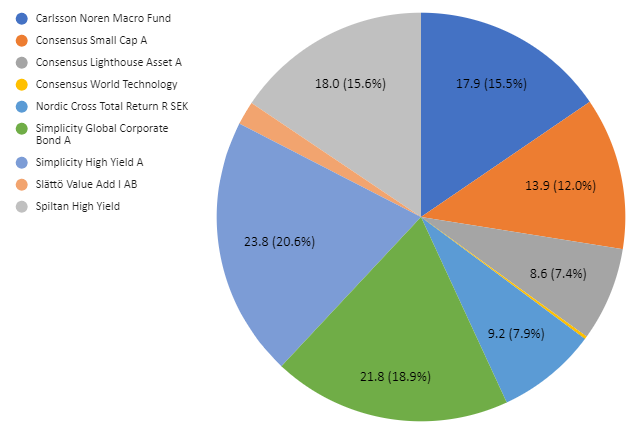

Finally, the latest balance sheet looks as follows. Total assets are about 240m, of which the largest line items are stocks and mutual funds of 115 m, and loans to credit institutions of 93 m. They have about 19 m in prepaid expenses, 2.5 m in bonds. The total debt is 80 m, but adjusting for their untaxed reserves of 44 m, the total debt is about 90 m (about 22% of the untaxed reserve is added to deferred tax, the rest is equity). After this adjustment, the debt is comprised of about 21 m in deferred tax, 3 m in other debt, 58 m in accrued expenses, and 7 m in dispositions. In other words, the net assets are 150 m, much of which is invested in mutual funds.

The line item stocks and shares of mutual funds is actually a little bit misleading, because as of the latest report (q3), this entire line item is comprised of investments in different mutual funds. Furthermore, most of this is invested bond funds. See the pie chart I created from the data in the report, where the fund, the value in million Consensus has allocated to it, and the percentage of the portfolio:

Segments

Going back to the topline, for the quarterly report, there is no footnote detailing the split between the segments, but there is in the 2020 annual report. Looking at the operating income split, it is clear that the massive boost in 2020 compared to 2019 came from the great performance in their actively managed funds. Compared to 2019, the only segment that had any significant growth was the income from fees on their funds. out of the 225 m in total provisions, 192 m came from fund fees. 14 m came from fees related to their stockbroking, and 15 m came from fees on their structured products. Compared to 2019, where stockbroking and structured products were both at about 15 m each, and fees on their funds were 35 m.

The Funds

Looking at this, it is abundantly clear that all of the incredible growth has come as a direct result of the incredible performance of the fund part of the business, more specifically, their small cap fund (which has a 200% return over the last three years). This leads us into the next segment, the funds:

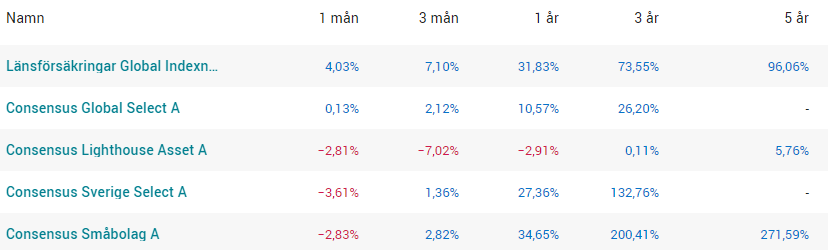

This table shows the returns for the Consensus managed funds, and the returns of a global low cost index fund. Comparing the funds, their AUM, and fee structure:

- Global select: 50 m sek AUM, 1.35% management fee and 20% performance based fee on the return above the MSCI World all cap index.

- Lighthouse: 300 m sek AUM, 1% management fee and 20% performance based fee on all positive returns.

- Sweden Select: 400 m sek AUM, 1.35% management fee and 20% performance based fee on the return above the OMXS all cap gross.

- Smallcap: 2 b sek under management, 1% management fee and 20% performance based fee on the return above the Swedish t-bill +3%.

Looking at the above, and the returns, it is clear that these are not cheap funds, and that the small cap fund dwarfs the others in terms of AUM. Looking at the performance based fees, I think having a small cap fund but taking 20% performance fee on the returns over the t-bill+3% is insane, but that’s just my two cents. It is also clear, that the fees from the small cap fund constitutes the vast majority of the income to Consensus, and here is where the case gets tricky.

Since the smallcap fund represents such a large part of the past earnings, let’s take a brief look at the current holdings of the fund.

- Hexatronic, 14% of portfolio, trailing P/E 78

- Embracer, 8%, P/E neg.

- Swedencare, 8%, P/E 146

- Physitrack, 6.5%, P/E neg.

- Evolution, 6.5%, P/E 45

- Plejd, 5.5%, P/E 118

- Awardit, 5%, P/E 152

- Carasent, 5%, P/E neg.

- Alcadon, 4.5%, P/E 45

- Better Collective, 4.5%, P/E 67

I am not going to go into each company any further, but I can say that most of these have been growing incredibly fast. Many have performed >100% year-on-year growth. So, it is very clear that the smallcap fund is probably more accurately categorized as a smallcap high growth fund.

Valuation

As I wrote earlier, market cap is about 500 m sek, and enterprise value is about 470 m sek. Comparing this to the first nine months operating profit, we get a multiple of about 6.6 times, and on an EV basis 6.3. Compared to the full year 2020 results, we get a multiple of less than 4, and a P/E of 6.4. Now, looking back at the chart at the top of this writeup, it is clear that 2020 and early 2021 are outlier events. Comparing the market cap to the 2019 full year results shows a sobering multiple of 43x operating profit, or a P/E of 90.

The price to net assets is 3.3.

So, should the smallcap fund repeat its insanely good 2020 (90%+ returns for 2020), then one can expect to see a huge increase again in both operating income, operating profit, net profit, and free cash flow. Consensus has no capex need so almost as much free cash flow that is generated can be paid out as dividends, or be reinvested.

Other Stuff

Consensus largest owner is the founder of the swedish car retailer Hedin Bil, Anders Hedin. The Hedin Bil Group controls the majority of shares (about 51%), highlighted in yellow. Patrik Soko is the current CEO, Claes-Göran Nilsson is the chairman, and Uwe Löffler sits on the board of directors.

One thing that I find “interesting” is that Anders Wright, the manager of Consensus Smallcap, has during 2020 sold a total of almost 25 m shares, for a total value of about 12.6 m SEK. Consensus commented the sale, stating that Wright sold because of “personal financial matters”, and state that he still holds 9.5 million shares, and is still highly engaged in the management and as manager of the fund, and “is therefore highly involved in the future development of the company”.

Conclusion

As it looks to me, Consensus at this valuation is a bet on the performance of the small cap fund. A downturn in growth stock valuations will probably hit the small cap fund very hard, but on the other hand, the companies have performed very well so far. I don’t really like the rest of the core business, as I think it is heavily reliant on hard-to-evaluate client relationships. So the business outside the funds should probably warrant quite a low multiple, and the returns from the funds (again the lion share is the smallcap fund) is very hard to guess.

So I am going to pass at the current valuation of 500 m, but I will keep it on the watchlist, potentially revisiting it at a lower valuation.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser.