For this edition I once again asked my followers on twitter to select one of three stocks, and Inwido was the winner. So here’s my write-up on Inwido, enjoy!

Business

Inwido is a Swedish company that offer windows, doors, and related products. They are active in most of Europe, but Scandinavia is the largest and most important geography. About 55% of revenue comes from Scandinavia, which is operated under brands such as Elitfönster, Hajom, Diplomat, KPK, Outline, and Lyssand-Frekhaug.

East and West Europe represent 24% and 8% of revenue respectively. Business is done under brands such as Pihla, Profin, Sokolka, CWG Choices, Allan Brothers, Jack Brundson, Carlson, and Dekko.

Finally, Inwido has a relatively young E-commerce business active in their largest markets. This is operated under brands such as JNA, Sparvinduer, Bedst & Billigst, and Bonusfönster.

Before listing on the Stockholm exchange in 2014, Inwido had quite a long history going back as far as 1811. Between 2000 and 2019 Inwido was acquiring companies and taking a market leading position in the Nordic region eventually branching out into Europe. In 2019 they employed a new governance strategy that is supposed to give the group companies more individual responsibility, which should result in a more decentralised organisation.

One very small note is that bad windows leads to more heat escaping, and in turn worse energy efficiency of the house. Better windows and doors should decrease the amount of energy that is wasted in a house. This is not special for Inwido but it should point to the importance of good windows and doors.

Financials

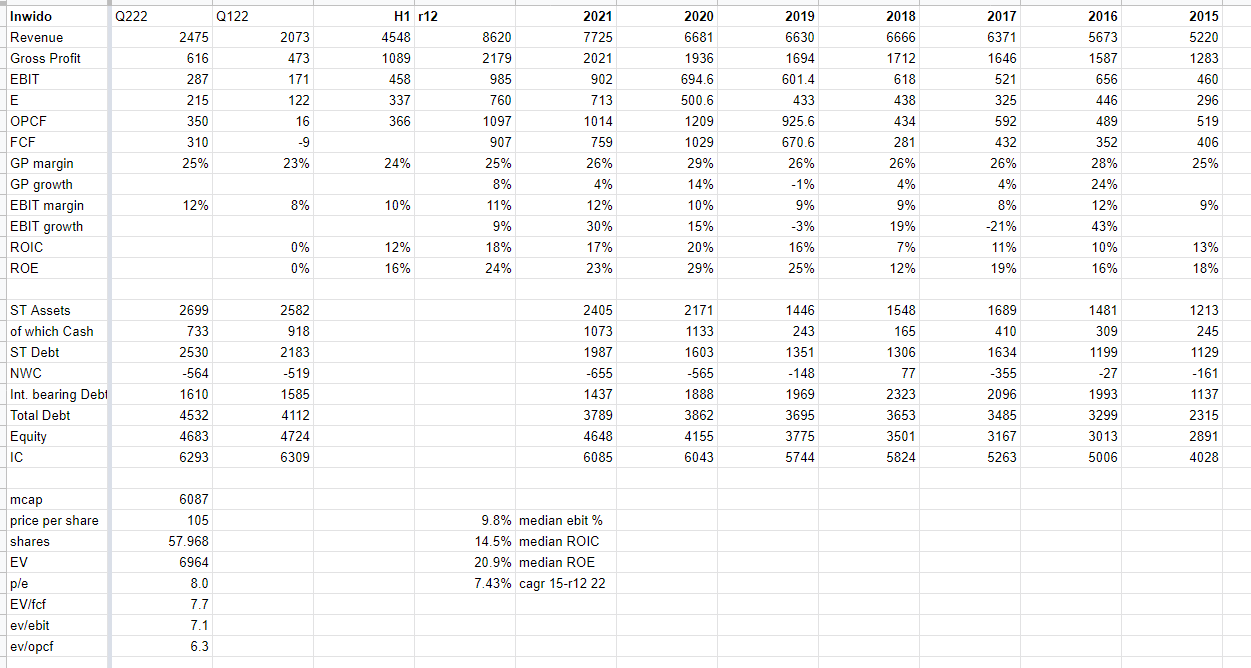

Looking at the financials from the first half of 2022 (Q1 + Q2), we have the following figures (m SEK):

Revenue: 4548

Gross profit: 1089

EBIT: 458

Net income: 337

Operating cash-flow: 366

This gives us a gross profit margin of 24% and an EBIT-margin of 10%.

The rolling 12 month figures are as follows:

Revenue: 8620

Gross profit: 2179

EBIT: 985

Net income: 760

Operating cash-flow: 1097

Gross profit margin is 25% and EBIT-margin is 11%.

The balance sheet is pretty good, with about 1.6 billion in interest bearing debt, 700 million in cash, and 4.6 billion in equity. The company operates with negative net working working capital, since they have about 2 billion in non-cash current assets and 2.5 billion in current liabilities. Their invested capital is about 6.3 billion, which gives us an approximate ROIC of about 18% and a return on equity of about 24%.

Looking from 2015 to the rolling 12-month period as of Q2 2022, Inwido has grown revenues by about 7.5% p.a, with a median margin of about 10%, median ROIC of 14% and finally a median ROE of over 20%.

Inwido’s financial targets are: to grow revenues faster than their underlying market, EBITA-margin of 12%, net debt to EBITDA < 2.5, and to have a dividend payout ratio of 50%. They do not specify how they are going to achieve this growth, so presumably they count with a mix of organic growth and acquisitions. The targets are not great, but they are not bad either. Better targets would be a growth rate and margin target that lands below the operating result, for example EBIT, or net earnings.

In order to not go needlessly in-depth and for the sake of brevity, I’ll put an image of some of the financials here. This summary should at least paint somewhat of a concise picture of Inwido.

Valuation

At a price per share of 105 SEK and with 57.968 million shares outstanding, we get a market capitalisation of about 6.1 billion SEK. With 1.6 billion in interest bearing debt and 733 million in cash, we get an enterprise value of close to 7 billion SEK.

Putting this in relation to the rolling 12-month income statement, we get the following multiples:

P/E: 8

EV/EBIT: 7

EV/OPCF: 6

Risks

The most currently relevant risks are a) weakening consumer, and b) the potential of a pandemic boosted business.

A weakening economy, and in turn a weakened consumer would likely lead to postponed plans regarding renovations, especially a big renovation like changing windows… A downturn in the economy also leads to fewer new construction starts, which also leads to fewer windows and doors sold.

Regarding b) I don’t really have much other than pure speculation. Maybe people, as they spent more time at home see that their windows are old, and decide to change them… Or as they spend more time at home realise that they want to live in a larger home and start construction on a new home? Maybe, I don’t know. So lets look at some scenarios:

Scenario 1. Revenue declines by 10% from pre-pandemic levels: This leads to a revenue of about 6 billion, and assuming a median EBIT-margin, we get about 600 million of EBIT. With the enterprise value of about 7 billion, this gives us an EV/EBIT of 11.7.

Scenario 2. Same revenue premises as in 1. but we use lowest margin I can find easily, 5.6% which happened in 2008: this gives us an EBIT of 336, and an EV/EBIT of about 21.

Conclusion

That Scenario 2 does not look great… But the first scenario looks ok to me. If revenue and margins are steady, at 7 billion in enterprise value we are getting a yield of about 14%. If they are correct about their growth, lets say 4%, and that they pay out half their earnings, we are getting about a 6% dividend yield, and a 4% growth. Remember that this 4% is lower than their historic growth, but maybe they have been “over-growing”, and are only going to grow at about market rate?

I don’t love owning construction related businesses right now, but I am fine with owning Inwido here. In short, I think the risk/reward is good here.

With that said, I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser. Both I and my significant other owns shares of Inwido at the time of writing this.