For this edition of ValueTeddy’s Writeups, I asked my twitter-followers to chose between Catella and North Media. Catella won by quite som margin, getting two thirds of the votes.

I first wrote about Catella about two years ago, at a price per share of about 21 sek. Between that post and today I have sold the shares I then held, and I have re-bought Catella, which is currently my third largest position. The old write up as of 10/08/2020 can be found here. What made me revisit the case was the best Swedish investing podcast in the world, Kvalitetsaktiepodden. In episode 107 (23/12/2021), Markus gives us a thorough explanation of the case in Catella (in Swedish). After hearing this episode, I decided to try my hand at valuing the company but landed at a much lower valuation than Markus. I sent him my figures and he was generous enough to type out a long and detailed email, where he explained what I was missing. That prompted me to make som adjustments in my figures and ended up finding about a 40% upside using quite defensive assumptions.

Brief Introduction

Catella is a real estate investment company consisting of three parts. This form is one that is quite recent, since Catella has undergone a multi-year change in business. For quite some time Catella was a bank, but then they decided that they wanted to get rid of their banking license. They tried selling it, but no buyers seemed interested, after which they decided to wind down the banking operation and eventually hand in the licence back to the Swedish regulators. This process was finally completed in Q4 of 2021. Along with handing in the banking licence, Catella also got rid of all their non-real estate hedge funds and mutual funds. The case in Catella has for the entirety of this process been that the new and fresh Catella would be worth more than before.

Now that this lengthy process is complete, I think this case is playing out favorably, and that there is considerable value in Catella.

The current version of Catella contains three parts: Investment Management, Principal Investments, and Corporate Finance. All three are solely engaged in real estate related business, and I will go through each one in detail.

Investment Management

This segment contains of investment funds focusing on real estate investments. Catella has several different funds, targeting pension managers, insurance companies, etc. They also offer asset- and property management under this segment. The total assets under managements are about 125 billion SEK as of Q1 2022, and the total revenue was about 1.1 billion. This gives us a fee of about 0.90%, which is in line with the median fee between 2019 and Q1 2022.

These funds should provide some sticky revenues, since the investors are frequently locked in for quite some time, compared to your standard mutual fund which often has daily liquidity.

The quarterly figures for this segment looks as below, but the most important figure, the median quarterly profit is about 47 m SEK.

Corporate Finance

The second operating part of Catella is their corporate finance division. This business “offers real estate companies, financial institutions, property funds and other property owners strategic advisory services, capital market-related services and high-end transaction advisory services”. This is a segment that fluctuates widely, and had a quite poor time during 2020-2021 due to fewer transactions.

In Q1 2022 the corp did 98 m SEK in revenue and reported an operating loss of 22 m SEK. The median quarterly operating profit between 2019 and Q1 2022 is 6 m SEK, and the quarterly figures are as follows.

Principal Investments

This is the most interesting part in my eyes, and a large part of the “hidden” values in Catella. This is the segment where Catella hold investments in properties. They are usually a part-owner in real estate projects, and they target an internal rate of return of about 20% on their investments. The interesting thing about this segment is that the company has said that 2022 will be a “harvesting year”, and especially H2 will be interesting.

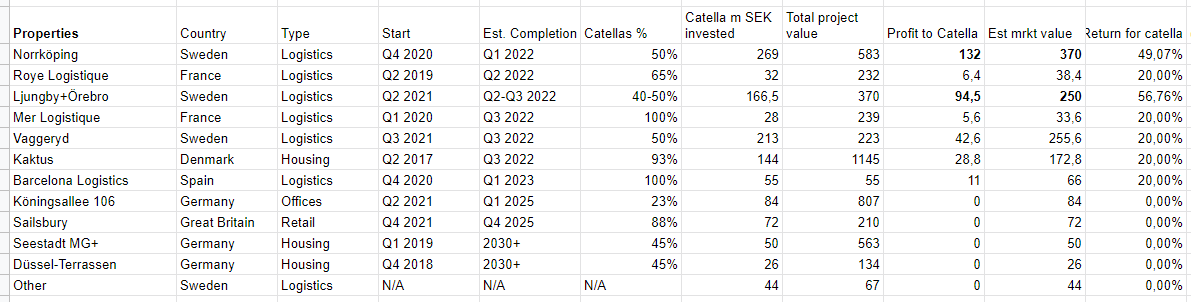

First of all, here is how I view their current investment property portfolio as of today (2022/07/11).

Looking at these properties, we can see a significant part of the portfolio is expected to be completed and sold during 2022.

The most important parts of this table are the expected completion, the SEK value that Catella has invested, and the expected return. These all tie into the estimated market value of Catellas share (“Est mrkt value” in the table).

The figures in bold refer to the fact that the Norrköping project and the projects Ljungby and Örebro have been sold. The returns for these are about 49% for Norrköping and 56% for Ljungby+Örebro. This is much higher than their target rate of 20%.

For the rest of the properties that are due before 2023, I have used the target IRR of 20%. For the rest of the portfolio, in the name of conservatism and margin of safety, I have used 0% return when calculating the value of the properties. Using this methodology, I have landed in a total value for the investment property portfolio at just less than 1.5 billion SEK.

Value of Operations

Adding together the Investment Management and the Corporate Finance parts, the median quarterly profit is about 67 m SEK between 2019 and Q1 2022. The average quarterly profit is lower, at 59 m SEK for the same period. Taking this lower figure times four gives an estimated annual run rate of just less than 240 m SEK.

When I first revisited Catella I felt that a multiple of 6x to 8x was fair. This values the operations to about 1500 to 1900 m SEK. However, after Markus from KAP made me realize that due to the stickyness of the capital invested in the funds, that part deserves a much higher multiple than 6-8. I think Markus uses a 15x multiple on the IM business, but I feel more comfortable using 12x for the combined IM and Corp operations. This values the operations at about 2900 m SEK.

Market Valuation

At 34 sek per share, Catella has a market cap of just north of 3 b SEK. With 2.65 b SEK of interest bearing debt, and about 1.1 b SEK in cash, we get an enterprise value of 4.55 b SEK.

The combined value of the operations and the investment properties total 4.4 b SEK. Looking at it this way makes Catella look fairly valued, but lets take another approach.

If we deduct the value I have ascribed to the investment properties from the EV, we get about 3 billion remaining. This is awfully close to the 2.9 b at which I valued the operaitons when using 12x as a multiple. Inversing this multiple gives us a yield of just above 8%. I don’t know if this helps, but it helps me in my thinking about the returns expected from an investment.

With fairly conservative assumptions, I am underwriting an 8% return on the operations at the current valuation. This still leaves me upside in Principal Investments, since there is reason to belive that some of the properties can net similar returns as the properties they have sold earlier this year.

Risks

Finally, the most important part. Since Catella now has a singular focus on real estate, they are quite reliant on the real estate market not completely drying up. IM is quite sticky and their investors are likely locked in for several years. But a longer downturn in real estate will mean outflows from the IM funds. But the corporate finance arm is dependent on transactions being made. No transactions means no revenues for CF. Also, if there are no bidders then Catella are unlikely to be able to get great returns on their long term investment properties.

This means that Catella is quite reliant on the european real estate cycle. In the short run, the interest rates are increasing, which should put a lid on the real estate. It should atleast slow the past few years incredible bull run in real estate valuations.

Concluding Remarks

First of all, if you are Swedish and have not yet done so: go and subscribe to Kvalitetsaktiepodden wherever you listen to podcasts. Thanks to Markus for so generously explaining how he sees Catella. The most important aspects of this case are: 1) the property investments that are due during 2022, and 2) the overall real estate transaction market.

Catella has been talking about 2022 being a “harvesting year” and given the great returns on their investments so far, I am very much looking forward to the rest of this harvest.

With that said, I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser. Both I and my SO owns shares of Catella at the time of writing this.