For this edition of ValueTeddy’s Write-Ups we are looking at a very cheap Korean game company called Gravity.

Business

Gravity is a Korean developer and publisher of online and mobile games. They were founded in 2000, and listed ADRs on NASDAQ in 2005. Gravity’s main IP is Ragnarok, which began with their first game: Ragnarok Online which launched in 2002. Ragnarok Online is an “online MMORPG”, and Gravity earns revenue from the subscription fee required to play. In some markets, Gravity licence the game, and thereby earning royalties and licence fees instead of subscription revenues. Even though it has close to 20 years behind it, Ragnarok Online contributed about 20% of the revenues in 2020 and about 10% of the 2019 revenues.

The largest part Gravity’s business is their mobile games. Gravity’s most important mobile game for 2020 was Ragnarok M: Eternal Love, followed by Ragnarok Origin. For 2020, Ragnarok M: Eternal Love represented 43% of Gravity’s total revenue, and Ragnarok Origin represented 17% of the total revenue.

During 2021, a new mobile game was released, Ragnarok X: Next Generation, which seems to have contributed significant amounts of revenue during 2020-09 to 2021-09.

Using data from Sensor Tower (H/T to @SickValue and @imnotdavey) and the latest filing (Q3 2021), I think the following is a somewhat accurate estimation of the share of total revenue for the last 12 months:

Ragnarok M: Eternal Love: 25%

Ragnarok Origin: 20%

Ragnarok X: Next Generation: 33%

Ragnarok Online: 18%

Other: 4%

Presumably, Other includes the games for various consoles, and Gravity NeoCyon, which develops “Hyper-Casual” games.

Upcoming titles

Ragnarok: The Lost Memories (mobile RPG), launching from Q3 2021 to Q2 2022

Ragnarok V: Returns (mobile MMORPG), launching from Q4 2021 to Q1 2022

Ragnarok Begins (cross platform MMORPG), beta in Q3 2021, no launch date

Project T (Tentative title) (mobile card game). expected launch in Q1 2022

Note that Gravity seems to launch games in only a few markets at a time, so these dates are approximate, and I guess that most of 2022 will include launches to new markets. One exception is Ragnarok Begins, which might be launched on all markets simultaneously. If this is the case, we will know when the launch date is announced.

I have no insights regarding the outlook for any of these titles, but we can look at some approximated costs for the development. The last three years (2020 to 2018) R&D expense has been the following (in KRW): 15 m, 9.5m, and 8 m. And the last 9 month R&D was 12 b KRW. The total R&D expense from 2018 to Q3 2021 is 44.5 b KRW. Compared to the last quarters (Q3 2021) gross profit of 37.7 b KRW, the R&D is basically peanuts. Furthermore, none of the development is capitalized, and the total intangible assets are about 3 b KRW.

In other words, should all these titles be complete failures, there wont be any write downs since all the R&D is already expensed and not capitalized. However, because of the finite lifetime of mobile games, the scenario where all these games are complete failures will cause revenue to eventually plummet, and this would in turn bring profits down with it.

In other-other words, Gravity has already taken all the development costs, which means there is no hidden downside should these games fail. But Gravity still gets to capture the possible upside should any of the games become a success. Gravity has already paid the cost, and gets to keep the positive optionality, instead of having the uncertain negative scenario of having to write down capitalized development costs.

Financials

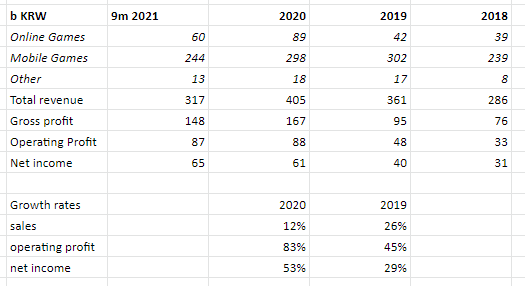

In this section I’ll do the financials in KRW, because that is the way they are reported in the 10-k for 2020. At the time of writing, 1 USD = 1197 KRW.

As we can see, Gravity is growing at a good pace, especially when looking at the operating profit and net income. It seems to me that the Ragnarok franchise still is able to bring in large sums, and that with low overhead costs, and very close to zero capex requirement.

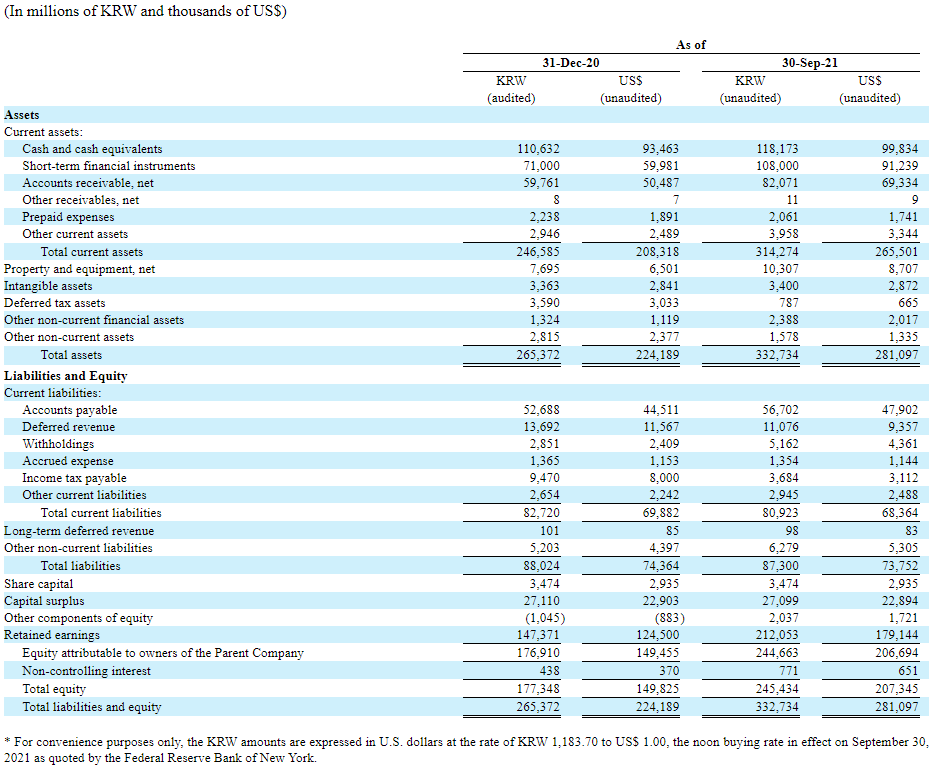

With that said, let’s look at the latest balance sheet:

Here it’s clear that Gravity has a great balance sheet. They have current assets, net of all debt, of 227 b KRW. Almost zero long term debt, and most of the assets are cash and short term investments. Finally, the balance sheet contains almost no intangible assets, or other assets where the value on the books would be very hard to determine.

With that said, moving on to the vaulation.

Valuation

Because all the financials are in KRW, I’m also going to convert the market cap to KRW. At 70 USD per share, the market cap is roughly 490 m USD, or 587 b KRW. Adjusting for the net current assets (again net of all debt, not just the short term debt), we get a very conservative EV of about 360 b KRW. This is just above 4 times the last 9 months operating profit.

In plain English, Gravity looks really cheap. By now we need to ask ourselves, why is Gravity so cheap?

Risks and Troubles

The Ownership Structure

The first risk/trouble I want to bring up under this segment is the ownership structure, and lack of insider ownership. Gravity’s majority shareholder is GungHo Online Entertainment, who own 59.3% of the company. GungHo’s largest shareholder is its founder, Taizo Son, the youngest brother of SoftBank founder Masayoshi Son. GungHo is the only shareholder above the 5% reporting threshold, and none of the managers of Gravity own any shares or ADRs in Gravity.

The relation between GungHo and Gravity started when Gravity originally launched Ragnarok Online, where GungHo was their licensee in Japan. In April of 2008 GungHo acquired about 52% of the shares outstanding in Gravity, and in June of the same year they purchased ADRs, further increasing their ownership stake to the current 59.3%.

Furthermore, the management in Gravity all hold significant positions at GungHo:

Hyun Chul Park, the CEO of Gravity, is General Manager at GungHo.

Yoshinori Kitamura, who is Chairman and COO of Gravity, is a Director and Executive General Manager at GungHo.

Kazuki Morishita, Executive director at Gravity is the President and CEO of GungHo.

And finally, Kazuya Sakai, Executive director at Gravity is a Director and the CFO of GungHo.

To me, this is unusual, and I don’t think I have ever come across a company, which is majority owned by one of its distributers, and where most of management are also managers of the distributor. And again, none of the managers of shares or ADRs in Gravity, and as far as I can tell, only Kazuki Morishita owns shares of GungHo (about 1% of the company).

Accounting

The second risk I want to discuss is something that jumped out at me when reading the 10-k for 2020, and it regards the accounting and audit of said 10-k. I was initially very alarmed at reading the following in the risk section of the report: “We have identified several material weaknesses in our internal control over financial reporting. If we fail to achieve and maintain an effective system of internal control over financial reporting, we may be unable to accurately report our financial results or do so on a timely basis, and our ability to prevent or detect fraud may be reduced, and investor confidence and the market price of our ADSs may be adversely affected.” This of course warranted further investigation, and what I understood from the auditors report is that these material weaknesses mainly regards how Gravity recognizes revenue. More specifically recognizing revenue from inactive players as deferred revenue.

Generally, concerns regarding a company’s accounting are huge red flags, because if you cant trust the figures you are getting from the report, then you have almost nothing to rely on for valuation. In the case of Gravity, the issues were only related to some things related to the calculation of the deferred revenue from inactive players. These following two points further solidify the fact that I do trust Gravity’s accounting enough to think that it is reliable for valuation:

1) Deferred revenue is an incredibly small part of the total liabilities on the balance sheet, and a full write down of the line item would only impact one quarters earnings. The total deferred revenue on the latest (Q3 2021) balance sheet totals 13.4 b KRW which is about half the net income for Q3 2021. This is also considered in the valuation, since deferred revenue appears as a liability, and thus increases the enterprise value.

2) The auditor states that the material weaknesses don’t change their opinion on the correctness of the financial statements.

Point 1 gives me enough reason not to worry about this risk, and point 2 slightly adds to this non-worry. If deferred revenue would have been a significant portion of the balance sheet, then the impact and likelihood of large impairments would have needed to be further evaluated.

Ragnarok

The third risk regarding Gravity I want to bring up is their reliance on only one IP, namely Ragnarok. To this I have nothing more to say than as long as it is selling, then this is fine. Having only one IP sure could cause some troubles, should that IP fall out of favour, and that might be cause for some discount. I do however think that the current discount on the stock relative to other mobile game companies out there, is far too big to be justified simply because of their singular IP.

A note regarding the Ragnarok IP is that the IP is not owned by Gravity, but they have the license to use it until 2033, after which the license will have to be renegotiated. Explanation from the 2020 10-k: “We obtained an exclusive license from Mr. Myoung‑Jin Lee to use the storyline and characters from his cartoon titled “Ragnarok” for the development of games including for animation and character merchandising. We paid Mr. Lee an initial license fee of Won 40 million and are required to pay royalties based on a percentage of adjusted revenues (net of value‑added taxes and certain other expenses) or net income generated from the use of the Ragnarok brand through January 2033.”

Capital allocation

The final, and most significant “trouble” in Gravity, is their capital allocation… Or rather, their lack of capital allocation. It seems that their capital allocation strategy is based around the notion that if you stack your coins, they wont roll away from you.

The combined investments in PP&E and intangibles from 2018 to 2020 are in total 7 b KRW. And As stated earlier, the total R&D from 2018 to Q3 2021 is 44.5 b KRW. There has been no dividends, no buybacks, and no significant acquisitions in the latest years. In other words, Gravity is just piling up cash. Their cash plus short term financial instruments almost doubled from 120 b KRW in Dec 2018, to 226 b KRW as of the Q3 2021 balance sheet.

This lack of active capital allocation could be one large part of the reason for the low multiple, but as the cash position keeps increasing, the EV decreases, which makes Gravity look even cheaper. The cash position is also an opportunity for Gravity to “unlock value” for shareholders, at the current valuation preferably through buybacks. Alternatively through an acquisition or other transaction. Note that guidance has been leaning towards acquisitions rather than buybacks of own shares. So even if buybacks would be good capital allocation, it is probably unlikely.

For more details about some of these risks, see the appendix. I also want to add that the 10-k is very thorough and offers very good explanations of the risks in Gravity.

Conclusion

To conclude this writeup, Gravity is obviously very cheap, but it does have its quirks. In short, I believe that the current multiple of about 4x operating profit with good margin compensates for a) the non-standard ownership structure and b) the lack of capital allocation.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser. At the time of writing, I own ADRs representing shares of Gravity.

Appendix, Cut-outs from the risk section in the 2020 10-k

GungHo, the licensee of our games in Japan, is our majority shareholder, which gives them control of our board of directors.

Since April 1, 2008, GungHo has been our largest shareholder and beneficially owns, as of the date hereof, 59.3% of our common shares. As a result, GungHo is able to exert significant control over all matters requiring shareholder approval, including the election of directors and approval of significant corporate transactions, including acquisitions, divestitures, strategic relationships and other matters, and may also exert significant control over decisions related to the status of our ADSs being eligible for quotation and trading on the NASDAQ Global Market. In addition, as GungHo is also an online and mobile game developer, there may be conflicts of interest. For instance, GungHo may lead our management with strategies and efforts which benefit itself, its affiliates and their respective shareholders to the detriment of our other shareholders. GungHo may also compete directly or indirectly against us for users and customers or increased market share for its games. GungHo is also currently the licensee of Ragnarok Online, Ragnarok M: Eternal Love and Ragnarok Origin in Japan. Furthermore, four of our Executive Directors, Mr. Hyun Chul Park, Mr. Yoshinori Kitamura, Mr. Kazuki Morishita and Mr. Kazuya Sakai currently serve as General Manager, Director and Executive General Manager, President and Chief Executive Officer, and Chief Financial Officer and Director, respectively, of GungHo, and there may be conflicts of interest in the decisions made by the Board of Directors of Gravity (the “Board of Directors”) and senior management.See ITEM 7.B. “RELATED PARTY TRANSACTIONS—Relationship with GungHo Online Entertainment, Inc.

—

We have identified several material weaknesses in our internal control over financial reporting. If we fail to achieve and maintain an effective system of internal control over financial reporting, we may be unable to accurately report our financial results or do so on a timely basis, and our ability to prevent or detect fraud may be reduced, and investor confidence and the market price of our ADSs may be adversely affected.

In connection with the preparation of our consolidated financial statements under IFRS for the year ended December 31, 2020, we have identified several material weaknesses (as defined under § 210.1-02 Definitions of terms used in Regulation S-X (17 CFR part 210)) in our system of internal control over financial reporting; our management assessed the effectiveness of our internal control over financial reporting as of December 31, 2020 pursuant to section 404 of the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley Act”) and related Securities and Exchange Commission (“SEC”) rules and concluded that our internal control over financial reporting was not effective as of December 31, 2020. See ITEM 15. “CONTROLS AND PROCEDURES.”

—

Deferred revenue-micro transaction

We sell virtual currency and in-game virtual items that can be used in online and mobile games to game users. For each game in each country, we estimate and apply the game user’s life cycle in order to recognize revenue generated by micro-transactions. The game user’s life cycle is estimated based on the average period from the game user’s first payment date to the last access date for active paying game users. We consider a game user as an active user if the period between the time of the user’s most recent access of the game and the end of reporting period equals or is shorter than the estimated game users’ life cycle. For remaining virtual currency, and in-game virtual items that active users own at period-end, the related revenue is deferred considering whether the virtual currency is refundable and items’ attributes. We estimate the user’s life cycle by analyzing game users’ activity patterns such as payment and access and it periodically reviews if there is any change of these estimates.