In this edition of ValueTeddy’s Write-ups we are examining a Swedish industrial high-quality business, trading at single digit multiples.

Business

AQ Group is a Swedish manufacturing company that was founded in 1994 and listed on the Stockholm exchange 2001. Their business is divided into two segments: Systems, and Components. Systems include the business divisions Electric Cabinets, and System products. The Components segment is made up by the following business units: Precision stamping and injection moulding, Inductive components, Wiring Systems, Sheet metal processing, and finally, Special Technologies and Engineering.

For 2020, Components represented about 80% of the total revenue, and about 66% of the operating and net profit. About 40% of the AQ Groups sales are made in Sweden, making it, by far, the largest market.

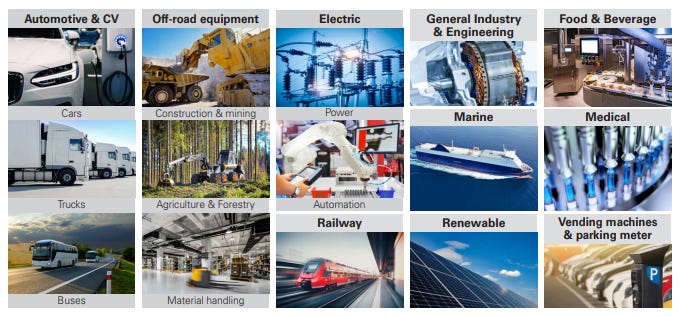

AQ delivers their products to a broad range of industries, broadly divided into five market segments: Automotive, Off-road equipment, Electric, Industry, and Food and Beverage. Each market segment constitutes three business areas, and AQ notes that “None of the 15 areas below is a dominating part of the net sales, our business is well distributed across these segments”. However, the two largest customers generate about 10% each of AQ Groups revenue.

Financials

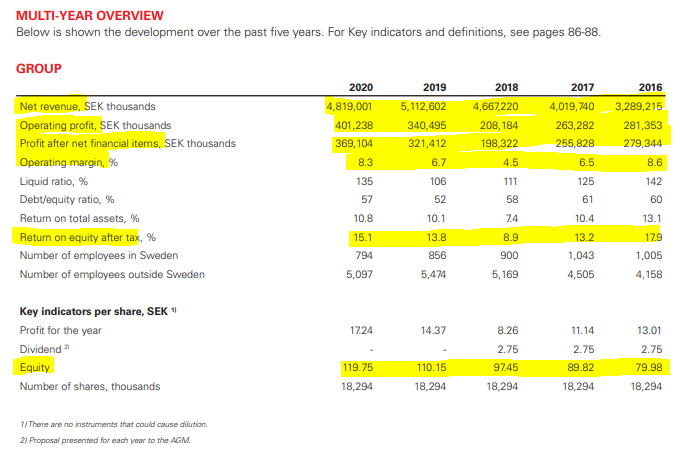

If we move to the financials, starting at the highlighted multi-year overview, we can see that sales has grown by about 45% from 2016 to 2020. The median operating margin is 6.5%, and the operating profit has grown by about 40%. The equity per share has grown by 50%. This translates to compounded annual growth rates between 7% and 8.5%.

Even though sales declined from 2019 to 2020, the operating profit increased, in turn increasing the margins.

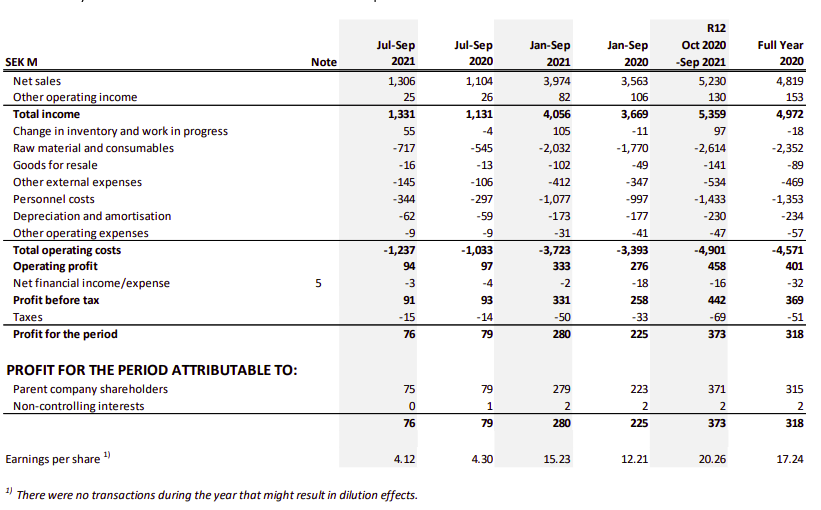

Looking at the income statement for Q1 to Q3 of 2021, we see similar developments as in the 5 year summary:

Sales broke the 2019-2020 development, and increased for Q1-Q3 for 2021 compared to the same period 2020. Operating profit and earnings per share followed suit. The growth in sales, operating profit, and earnings was 10%, 20%, and 24% respectively.

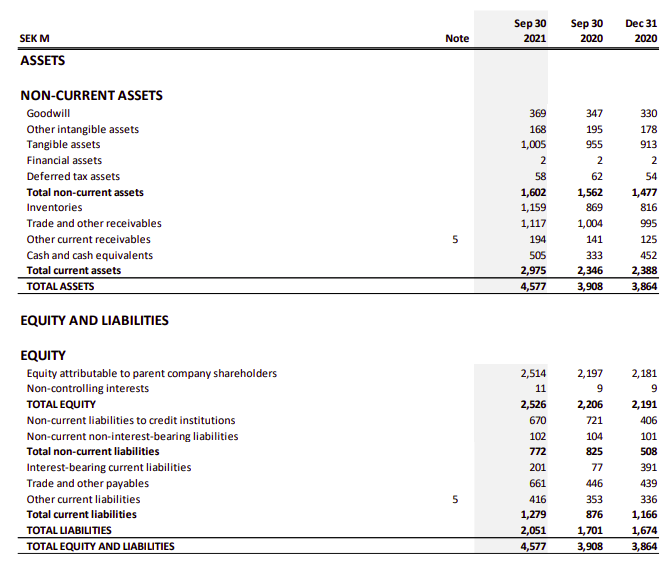

The latest balance sheet looks as follows:

There is almost no goodwill or other intangibles on the asset side, tangible fixed assets total 1 billion SEK, total current assets total just short of 3 billion, and about 500 m of this is cash. The total liabilities are just north of 2 billion, and of this debt only 870 m is interest bearing. Current debt is more than twice covered by current assets, and the company is generally conservatively financed with net tangible assets of 2 billion SEK.

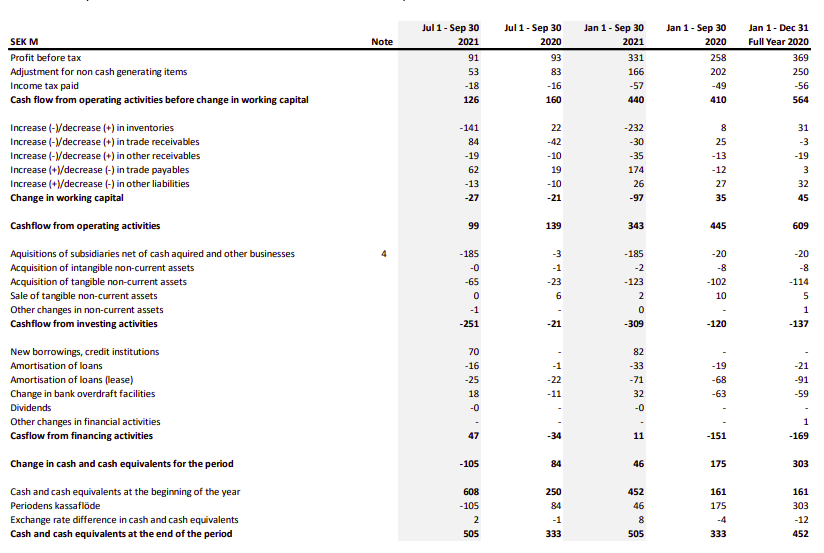

Finally, the cash flows:

Looking at the first nine months of 2021, the business generated about 340 m of operating cash flow, of which about 300 m was reinvested in the business. On the financing side it looks like they rolled some loans.

Looking forward

I think the maintenance capital expenditures should be quite close to depreciation, and that the operating cash flow generation should be quite close to operating income before depreciation and amortization. In other words, I believe that free cash flow should be about 40-50% above operating profit, or close to 10% of sales.

Given the diverse industries AQ Group serves, and looking at the historical operating performance, I believe these historical figures are quite a decent guide for the future. I think AQ can grow by 5% to 10% annually, while maintaining their operating margins of 4% to 8%. I also believe that the free cash flow that is generated can be reinvested at close to the return on equity for AQ. I don’t think there is risk that management will waste the cash flow on poor investments or by overpaying for acquisitions.

Here it is important to note that AQ has no target regarding growth above Earnings before Tax. In other words, it is unlikely that they will go on an acquisition spree in order to boost sales, EBITDA, EBITA, or any other non-GAAP measure. Furthermore, they have a conservative history, not issuing shares, and paying some of its earnings as a dividend. Note that this dividend was cut for 2019, after first postponing the annual meeting (scheduled for Q1 2020 to Q2 2020), and there was no dividend for 2020. I think this is purely out of caution, and they cite in their press releases during this period that it is difficult to foresee the impact of the Covid-19 pandemic on AQ. We can see with hindsight that they handled the pandemic with good results, as the earnings per share increased significantly, and that the equity and operating profit also increased.

Valuation

At a price per share of 300 SEK, and a share count of 18.294 m, the market cap is just less than 5.5 billion SEK. Adding the total interest bearing debt of just less than 900 million, and deducting the 500 million of cash on the balance sheet, we get an enterprise value of 5.9 billion.

Comparing this to the 2020 operating profit of 400 million, gives us an EV/EBIT multiple of about 15, and compared to the rolling 12 months operating profit of 458 from the Q3 report we get a multiple of 13.

If we use the 2020 years sales numbers, and the five-year lowest operating margin of 4,5%, we get an operating profit of about 215 million, which gives us an EV/EBIT of about 27.

Using the trailing 12 months earnings from the Q3 report of 373 million, we get a P/E of just less than 15.

Other

Both founders, Claes Mellgren and Per Olof Andersson own about 25% of the shares each bringing their total shares to 49.40% of the shares.

Being an industrial company, AQ Group should follow the business cycle pretty closely, meaning that if business slow down, they should face declining sales, and as general business is good, then AQ should do pretty well. One huge strength for AQ is their conservative balance sheet and their responsible and relatively careful management, which should let AQ have better odds of surviving a prolonged slowdown in the general economy than the average industrial peer.

Conclusion

I am very positive on the risk/reward regarding AQ here. Even if operating margins contract, it is not that expensive. I like that the founders still own significant shares, and I like their sound and reasonable financial goals.

I see both upside in the prospective growth at above-inflation levels, and downside protection given the very low multiple. AQ Group has other industrial peers trading at absolutely ridiculous valuations (bound to come down), but AQ is still traded at very low multiples. I don’t see any reason for AQ to trade at any sort of discount, as the quality of the business is very good.

I hope you liked this edition of ValueTeddy’s Write-ups! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser. AQ Group represents about 15% of my portfolio at the time of writing.

Edit after original post: the valuation section has been rewritten after receiving valuable feedback from friends on Twitter and sharp readers of this Substack. The original text understated the enterprise value by calculating it without consideration of going concern, which is something I blame on doing too much SOTP cases in recent times. Thanks for the feedback.